Decentralized vs centralized exchanges

Decentralized vs centralized exchanges compared. Custody, fees, access, transparency, and the structural trade-offs that define how each model serves traders.

Introduction

Sunday morning. A central bank in Asia announces an emergency rate decision. Crypto markets move. Equity index futures crack. The dollar shifts. Two traders open their apps. One sees a maintenance banner across their centralized exchange. The other signs a transaction and is in position within seconds. By the time the first platform comes back online, the move is done. Same news, same chart, completely different outcomes. The infrastructure was the difference.

This is the era we're trading in now. Centralized exchanges have decades of infrastructure behind them and trillions of dollars of volume. Decentralized exchanges have caught up faster than most traders realize, and now match or exceed centralized exchanges on every dimension that used to be a clear CEX advantage. The choice between the two is no longer about convenience vs principles. It's about which infrastructure actually serves your trading.

Custody, fees, access. That's the real difference. Every other comparison flows downstream from those three. Centralized exchanges hold your funds, set their fees with hidden spreads, and gate access by jurisdiction and identity. Decentralized exchanges leave funds in your own wallet, settle on-chain with transparent fees, and accept any wallet that connects. Once you understand what each model actually does, the choice becomes structural, not preferential.

This guide walks through the full comparison. What each model is, how they differ structurally, how trading actually feels on each, where each one fails, what assets you can trade on each, where modern platforms sit on the spectrum between the two, and which model fits which trader. By the end, you'll have a clear framework for choosing the right venue for the size and strategy you trade.

We’ll also cover how the lines are blurring as on-chain order-book infrastructure and trading terminals emerge, combining the structural advantages of decentralized rails with the execution quality previously associated only with centralized venues. The CEX vs DEX debate that dominated crypto trading for a decade is becoming a different debate entirely. The question is no longer which model has stronger features. It's whether the platform you trade on holds your funds or you do, and whether its execution can be independently verified or not.

What is a centralized exchange?

A centralized exchange is a private company that operates a trading platform. The company runs the matching engine, holds user funds in exchange-controlled wallets, manages the order book, and settles trades on its internal ledger. Users deposit funds, trade against the exchange's book, and withdraw when they want their funds back. The exchange is the trusted intermediary at every step of the process.

This is the model most traders are familiar with. Binance, Coinbase, Kraken, Bybit, eToro. All centralized exchanges. The user-facing experience is polished. Liquidity on major pairs is deep. Execution is fast. The company handles all the complexity of running a trading venue, and the user trusts that they're handling it correctly.

Centralized exchanges do real things well. They aggregate liquidity. They provide regulated on-ramps from fiat. They offer customer support, fraud protection at the operational level, and a familiar account-based experience. For new traders, the friction is low. For traders who never want to think about wallet security or transaction signing, the trade-off is straightforward. You give up custody and get convenience.

What is a decentralized exchange?

A decentralized exchange is a trading venue where custody, settlement, and core trading activity are handled through blockchain infrastructure rather than a traditional exchange-controlled ledger. Depending on the design, execution may happen through AMM pools, on-chain order books, or appchain-based trading systems. The common thread is that users interact through wallets instead of depositing funds into a centralized exchange account.

The first generation of DEXs were AMMs. Uniswap, Curve, Balancer. They replaced the order book with a liquidity pool, used a mathematical formula to set prices, and let anyone trade by swapping against the pool. They solved the custody problem and the access problem, but they had real execution limitations. No limit orders. Slippage that scaled with trade size. Gas costs that made small trades uneconomic on congested chains.

The next generation closed many of those gaps. Platforms like GMX and early dYdX brought decentralized perpetuals into a more professional trading format, with leverage, deeper liquidity, and infrastructure designed specifically for active traders. dYdX started on StarkEx, a Layer 2 scaling system, before moving to its own appchain with dYdX v4. Hyperliquid represents the next step after that: a purpose-built Layer 1 with an on-chain order book, native matching engine, professional market makers, full order types including stops and limits, and execution speeds much closer to centralized exchanges. The DEX category today is not the DEX category of 2020.

The defining feature across decentralized trading systems is wallet-based custody. Users do not deposit assets into an exchange-controlled account or rely on a centralized company to process withdrawals. Depending on the protocol, collateral may be posted to smart contracts or trading accounts, but the custody model is still fundamentally different from a centralized exchange: access is wallet-based, settlement is on-chain, and there is no pooled exchange wallet standing between the trader and the system.

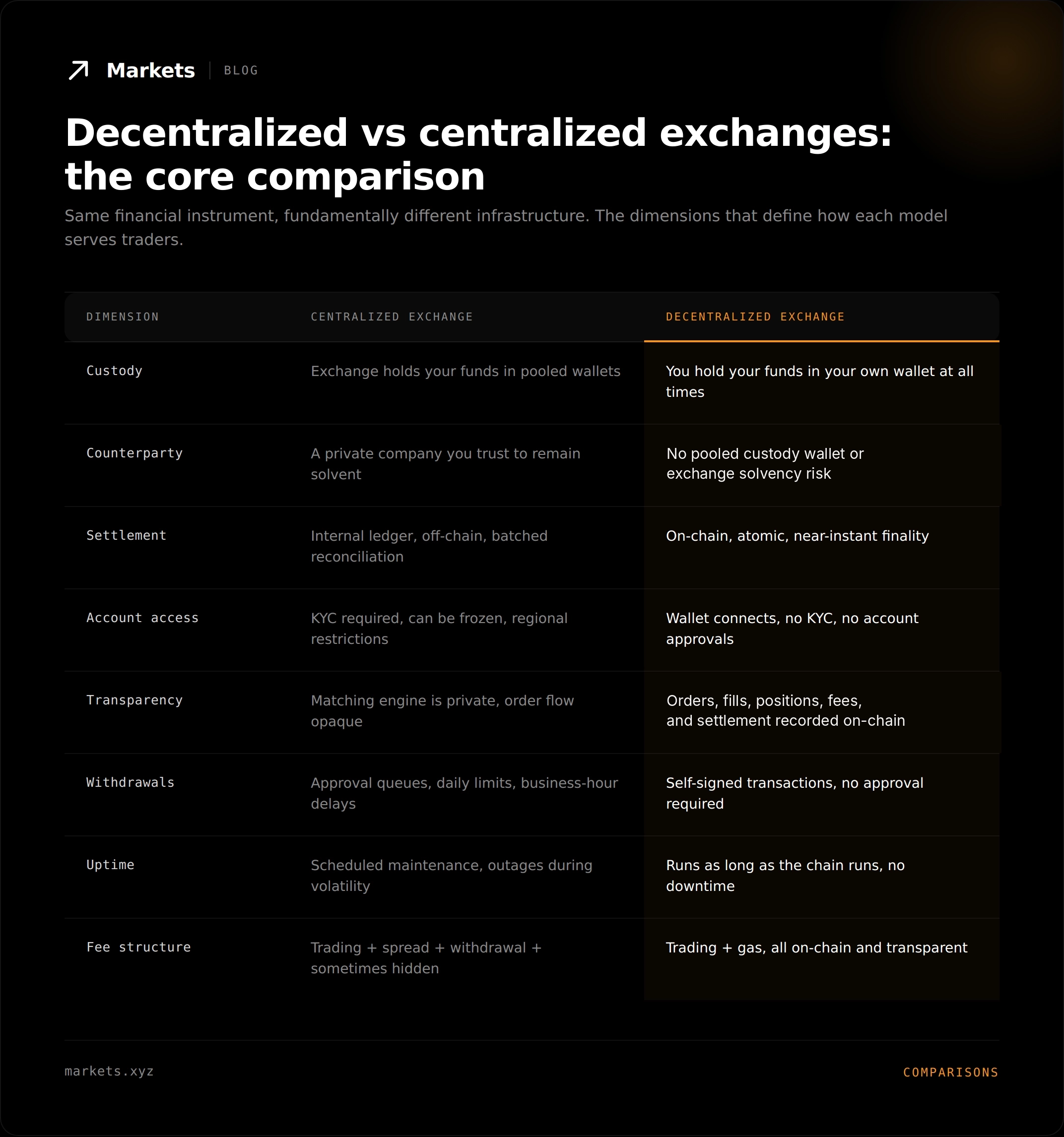

The structural differences that actually matter

Most CEX vs DEX comparisons get lost in surface details. The differences that actually shape the trading experience and the risk profile come down to four dimensions. Custody, fees, access, and transparency. Get clear on those four and the rest follows.

Custody (the biggest difference)

On a centralized exchange, when you deposit funds, they leave your control the moment you hit confirm. The exchange holds the underlying assets in pooled wallets. Legally and operationally, those funds belong to the exchange while they're on the platform. You hold a claim against the exchange, not the assets themselves. If the exchange fails, you're a creditor in bankruptcy proceedings. FTX users learned this. Mt. Gox users learned this. Celsius users learned this. The pattern repeats because the underlying model has not changed.

On a decentralized exchange with self-custody, your funds remain in your own wallet throughout the trade lifecycle. The smart contract has permission to execute trades on your behalf, but it cannot redirect funds, freeze your balance, or impose withdrawal limits. There is no platform-level custody risk because the platform never takes custody. This is not a marketing distinction. It's the single largest structural difference between the two models, and it determines how every other risk gets evaluated.

Fees and economics

Centralized exchange fees are usually higher than they appear. The headline trading fee is the visible cost. The hidden costs include the spread the exchange takes on quoted prices, the withdrawal fee that often exceeds actual network costs, the funding rate spread on perpetuals, and various smaller charges that add up over a trading year. Many CEXs run effective fee structures that are 2 to 3 times the headline rate once everything is counted.

Decentralized exchanges run leaner economics by structure. Trading fees go to the protocol or to liquidity providers. There's no company overhead to fund, no compliance team to pay for, no marketing budget extracted from fees. Withdrawals are on-chain transactions you pay gas for, with no platform markup. On modern DEXs built for active trading, total all-in costs are often meaningfully lower than the comparable CEX, even for active traders running high turnover.

Access and KYC requirements

Centralized exchanges require KYC. They restrict access by country. They set tier-based limits on withdrawals, trade sizes, and features based on verification level. They can deny service, freeze accounts, or suspend withdrawals at their own discretion or under regulatory pressure. From the exchange's perspective, this is operational reality. From the trader's perspective, it means access can be revoked at any time for reasons that have nothing to do with the trader's own behavior.

Decentralized exchanges accept any wallet. No KYC at the protocol level. No regional restrictions on the underlying smart contracts. Front-end interfaces may apply geographic restrictions for compliance reasons, but the protocol itself remains accessible. This is what enables genuinely global trading access. A trader in Lagos, São Paulo, Manila, or Mumbai has the same access as a trader in London or Singapore. The wallet is the credential.

Transparency and verifiability

Centralized exchanges are black boxes. The matching engine runs on private servers. The order book is what the exchange says it is. The proof of reserves attestations many exchanges now publish are point-in-time snapshots, not continuous verification. Whether the exchange is frontrunning user orders, whether market makers get preferential treatment, whether the displayed liquidity actually exists, are all things you take on faith. The exchange has every incentive to look trustworthy and few structural mechanisms to verify it.

Decentralized exchanges make the trading system far more verifiable. The key activity happens on-chain: orders, fills, positions, fees, liquidations, balances, and settlement can be inspected directly instead of relying only on an exchange’s internal database. That does not mean every part of every DEX is fully open source, and it does not mean there is no trust involved. It means the most important parts of the trading lifecycle leave a public, permanent record. The trust model changes from “believe the exchange” to “verify the system’s state and activity.”

Self-custody, transparent execution, no gatekeepers. Start trading on markets.xyz.

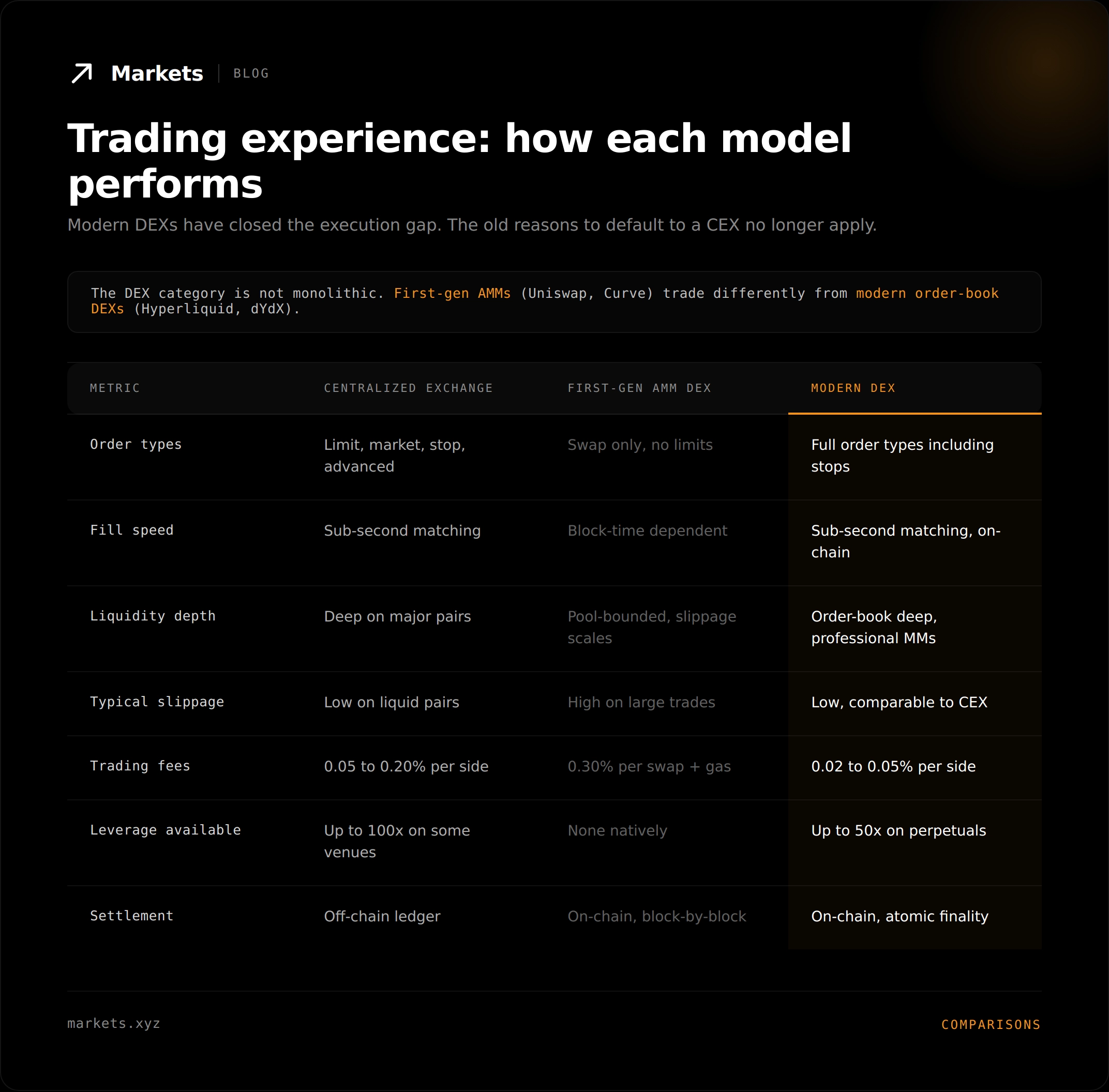

Trading experience: how each model performs

For most of crypto's history, the trade-off was real. Centralized exchanges offered better execution, deeper liquidity, and faster fills. Decentralized exchanges offered self-custody and transparency, at the cost of slippage, speed, and limited order types. Choosing meant accepting the trade. That stopped being true around 2023. The modern DEX category executes at parity or better with centralized exchanges across every dimension that matters for active trading.

Order execution and matching speed

Centralized exchanges match orders in sub-second windows on private servers. First-generation AMM DEXs matched orders at block speed, with each transaction waiting for the next block to confirm. For active trading, the gap was real. Modern DEXs built on trading-specific chains close it almost entirely. Hyperliquid, for example, runs sub-second on-chain matching with HyperBFT consensus, which means order execution speed is no longer a meaningful difference.

Liquidity depth and order book quality

Liquidity used to be the strongest argument for CEXs. Binance and Coinbase had the deepest books, the tightest spreads, and the most active market makers. AMM DEXs depended on whatever liquidity providers had pooled, which capped effective trade size. Modern DEXs with on-chain order books have changed this. Professional market makers now run on decentralized platforms with the same depth they bring to centralized venues, because the infrastructure can support it.

On a major pair like BTC or ETH, the spread and depth on a leading modern DEX is comparable to a top-tier CEX. On longer-tail assets, the picture is more mixed. Some DEXs have deeper niche-asset liquidity than CEXs because the asset is native to the chain. Others are still building. The gap that used to exist as a category is now a per-asset question.

Slippage, fees, and the all-in cost of trading

Slippage on a first-gen AMM scales with trade size and the depth of the liquidity pool. Large trades push the price along the curve and create execution costs that don't exist on order-book venues. Modern order-book DEXs eliminate this. Slippage on a deep on-chain order book is comparable to slippage on a CEX of similar liquidity, which is usually negligible for retail-sized trades and competitive even for institutional sizes.

Fees vary by venue but the modern DEX cost structure is generally lower. Trading fees of 0.02 to 0.05% per side are common, versus 0.05 to 0.20% on most CEXs. There's no withdrawal markup. There's no spread tax on execution. For active traders, the cost difference compounds across thousands of trades per year. For passive traders, it shows up in cleaner entry and exit pricing.

Where DEXs used to lose, and how they caught up

Three years ago, the gap between CEX and DEX execution was a genuine reason to use a CEX. Order matching speed, liquidity depth, available order types, leverage, and asset breadth all favored centralized venues. The DEX user gave up real performance for self-custody. Today, modern DEXs offer full limit and stop order types, perpetuals with up to 50x leverage, sub-second matching, and depth that matches major CEXs on core assets. The gap is gone for any trade size most retail and most institutional traders run.

What hasn't gone away is the structural advantage of self-custody and transparency. The CEX cannot eliminate its custodial risk. The DEX cannot be hacked at the pooled-wallet level because there is no pooled wallet. These aren't features that can be added or removed. They're consequences of the architecture.

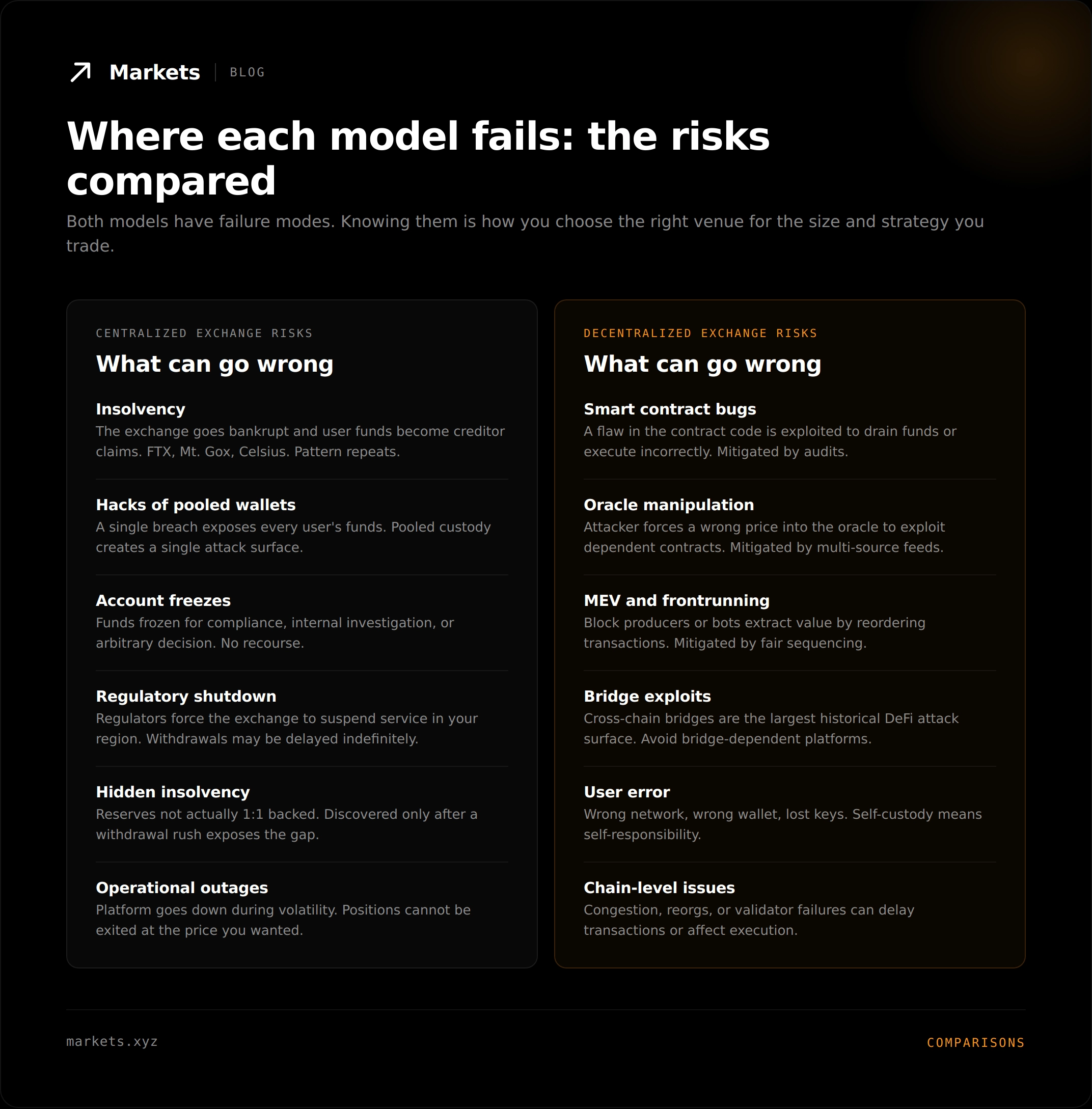

Where each model fails: the risks compared

Both models have failure modes. Honest evaluation means understanding what can go wrong on each, how likely each failure is, and how to evaluate platforms within each category. No platform is risk-free. The question is which risks you'd rather take and which mitigations the platform actually has in place.

CEX failure modes

Centralized exchanges fail in predictable patterns. Insolvency, where the exchange becomes bankrupt and user funds become creditor claims. Hacks of pooled wallets, where a single breach exposes every user's balance. Account freezes for compliance, internal investigation, or arbitrary decisions with no recourse. Regulatory shutdowns that suspend service in your region or indefinitely. Hidden insolvency, where reserves are not actually 1:1 backed and the gap is discovered only after a withdrawal rush. Operational outages during volatility when positions cannot be exited.

Each of these failures has historical examples. FTX, Mt. Gox, Celsius, Voyager, BlockFi, QuadrigaCX. The list goes on. The pattern is not random. The model creates the failure modes. Pooled custody creates the single attack surface. Centralized control creates the freeze risk. Off-chain settlement creates the reconciliation gap that hidden insolvency exploits. Choosing a CEX means accepting these risks and trusting the specific platform to manage them well.

DEX risk profile

Decentralized exchanges have a different set of risks. Smart contract bugs, where a flaw in the contract code is exploited. Oracle manipulation, where an attacker forces a wrong price into the price feed. MEV and frontrunning, where block producers or bots extract value by reordering transactions. Bridge exploits, which are historically the largest single attack surface in DeFi. User error, where wrong networks, wrong wallets, or lost keys create losses that nobody can reverse. Chain-level issues like congestion, reorgs, or validator failures.

These risks are real but generally more bounded than CEX risks. A smart contract bug affects users who interact with the buggy contract, not every user of the platform. Oracle manipulation typically affects specific positions, not pooled balances. Self-custody means user error replaces operator error, which is a different kind of risk but one the trader has direct control over. For evaluating platforms, the audit history, oracle architecture, and chain choice tell most of the story.

How to evaluate either category

For a centralized exchange, evaluate the regulatory standing, the proof of reserves quality and frequency, the platform's track record during volatility, the withdrawal experience, and the legal jurisdiction the exchange operates under. Strong CEXs publish frequent attestations, maintain clean regulatory standing, and have transparent fee structures. Weak CEXs hide behind marketing and resist questions about how reserves are actually held.

For a decentralized exchange, evaluate the audit history, the oracle architecture, the underlying chain's track record, the team's response to past incidents, and the active value at stake in the contracts. Strong DEXs have multiple independent audits, multi-source oracles with defensible mitigations, mature codebases that have been live with significant TVL for many months, and clear documentation of how risks are handled. Weak DEXs launch fast, audit lightly, and hope nothing goes wrong.

Asset coverage and what you can actually trade

What assets you can trade matters as much as how you trade them. The CEX vs DEX comparison on asset breadth has shifted dramatically over the past two years, with modern DEXs now offering coverage that used to be a CEX exclusive.

CEX asset breadth

Top centralized exchanges typically offer hundreds of spot trading pairs, a wide range of futures and perpetuals contracts, some options, and on a few of the largest platforms, traditional assets like equities, indices, and commodities via tokenized or derivative wrappers. The asset breadth is genuine and meaningful. For traders who want one venue covering everything from BTC to tokenized US500 to gold to FX, the leading CEXs have historically been the only practical option.

DEX asset breadth

First-generation DEXs were crypto-only. AMM-based platforms focused on the long tail of crypto assets, where on-chain liquidity actually existed. Modern DEXs have expanded significantly. Hyperliquid offers perpetuals across most major crypto assets with deep liquidity. Markets.xyz extends that further to cover equities, indices, commodities, and FX, all 24/7 on the same chain, with self-custody throughout. The CEX exclusivity on non-crypto assets is gone for any trader willing to use a modern smart contract platform.

The 24/7 cross-asset advantage of modern DEXs

What modern DEXs offer that centralized exchanges structurally cannot is genuine 24/7 access across every asset class. CEXs that offer tokenized equities typically restrict trading to traditional market hours, because their oracle infrastructure and settlement processes depend on the underlying market being open. DEXs with continuous oracle pricing trade every asset, every hour, every day. This is the asymmetry that defines the next era of trading platforms.

For a trader who wants to react to weekend macro events, position around after-hours earnings shocks, or hedge equity exposure on a Sunday morning, the only viable infrastructure is a smart contract platform with continuous oracle pricing. The traditional CEX model cannot deliver this because it depends on traditional venues being open. The DEX model removes that dependency at the architectural level. It's not a feature that CEXs will eventually add. It's a structural difference in how the two models are built.

Trade crypto, equities, indices, FX, and commodities on one decentralized platform, 24/7. Start trading on markets.xyz.

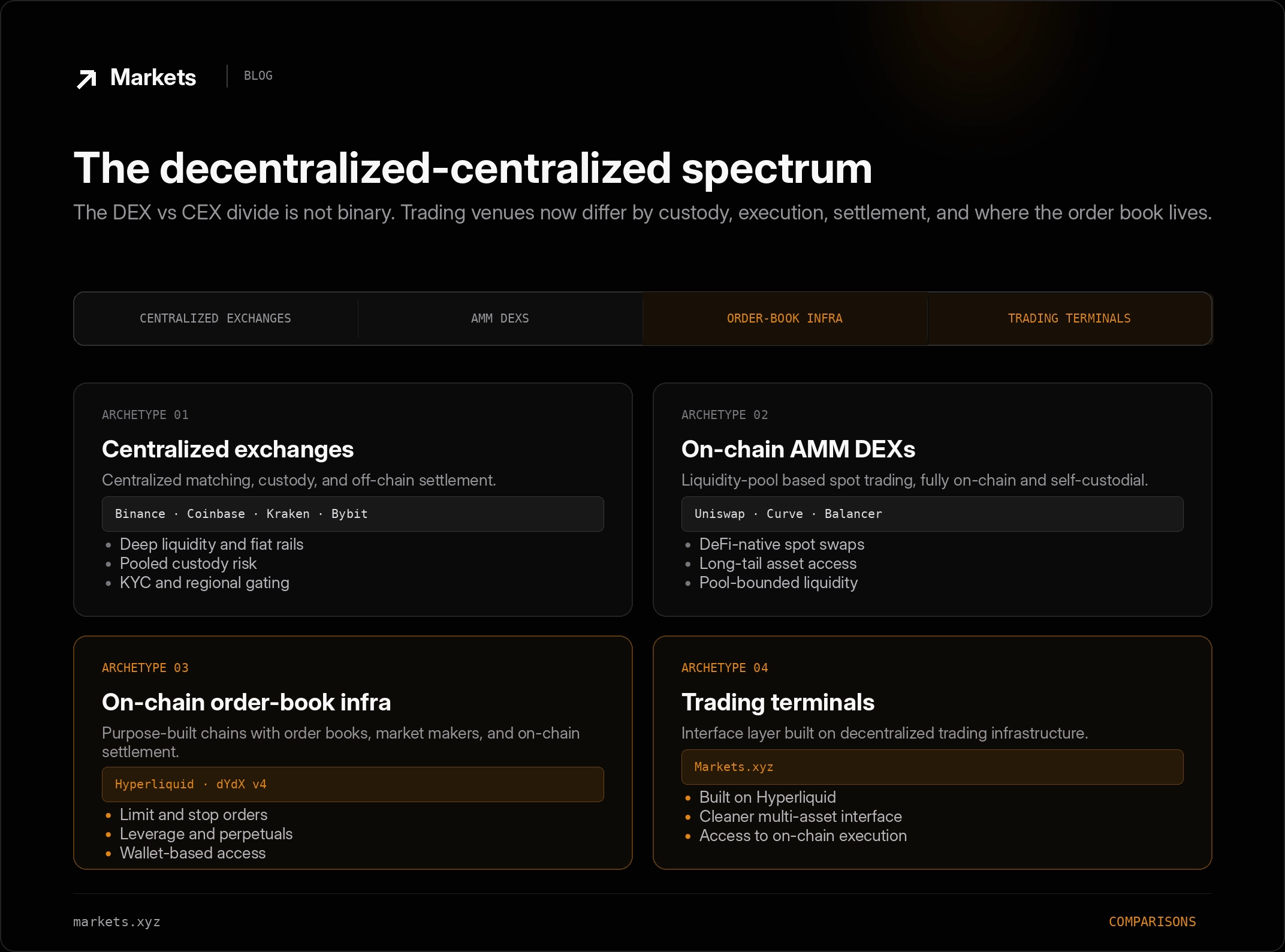

The decentralized-centralized spectrum

Treating decentralized exchanges vs centralized exchanges as a strict binary misses where trading infrastructure has actually moved. The market is no longer split only between fully centralized exchanges and early on-chain AMMs. There is now a broader spectrum of trading venues, defined by custody, execution, settlement, and where the order book lives.

Pure CEXs

At one end are centralized exchanges like Binance, Coinbase, Kraken, and Bybit. These platforms run centralized matching engines, hold user funds in exchange-controlled wallets, and settle trades on internal databases. They offer deep liquidity, familiar account-based onboarding, fiat rails, and strong execution on major markets.

The trade-off is structural. Users do not control their funds while trading. Order matching happens inside a private system. Withdrawals depend on the exchange. Access depends on jurisdiction, account status, and KYC approval. For many traders, centralized exchanges remain useful for fiat on-ramps and basic account-based trading, but the model comes with counterparty risk by design.

On-chain AMM DEXs

The first major wave of decentralized exchanges was built around automated market makers. Platforms like Uniswap, Curve, and Balancer replaced centralized order books with liquidity pools and smart contracts. Traders swapped directly against pooled liquidity, while liquidity providers earned fees for supplying assets to the pool.

This model made decentralized trading work at scale for spot crypto assets. It solved custody and access problems, opened long-tail token markets, and became one of the core primitives of DeFi. But AMMs are not optimized for every type of trading. Slippage increases with trade size, execution depends on pool depth, advanced order types are limited, and the model is not ideal for high-frequency, leveraged, or professional order-book trading.

AMM DEXs remain important, especially for DeFi-native spot trading and long-tail assets. But they are not the endpoint of decentralized exchange design. They are one branch of the DEX market.

On-chain order-book infrastructure

The next category is on-chain order-book infrastructure. This is where platforms like Hyperliquid and dYdX v4 sit. Instead of using an AMM pool as the execution layer, these systems use order books, professional market makers, purpose-built chain infrastructure, and on-chain settlement.

This category is closer to centralized exchanges in trading experience, but very different in structure. Traders get limit orders, stop orders, leverage, perpetuals, deep liquidity, and fast execution, while keeping wallet-based access and on-chain settlement. The goal is not to make an AMM more efficient. The goal is to rebuild the professional exchange stack on crypto-native infrastructure.

Hyperliquid is the clearest example of this shift: a purpose-built Layer 1 designed around an on-chain order book and trading-first infrastructure. dYdX v4 follows a similar direction through its own appchain. These platforms are not “DEXs” in the old AMM sense. They are decentralized trading infrastructure for active markets.

Trading terminals built on decentralized infrastructure

A separate category sits above the base trading infrastructure: trading terminals and apps built on top of decentralized rails. This is where Markets.xyz fits.

Markets.xyz is not the base DEX itself. It is a trading terminal built on top of Hyperliquid infrastructure. The terminal gives traders access to on-chain execution, wallet-based access, and Hyperliquid’s trading stack through a cleaner multi-asset interface. The user-facing experience can feel closer to a modern trading app, but the underlying execution model is still built around decentralized infrastructure.

Hyperliquid is the underlying trading infrastructure. Markets.xyz is the interface and product layer that makes that infrastructure usable across crypto, equities, indices, commodities, and FX. In the same way that professional traders often choose terminals based on workflow, speed, market coverage, and interface quality, traders can choose Markets.xyz as the terminal through which they access on-chain markets.

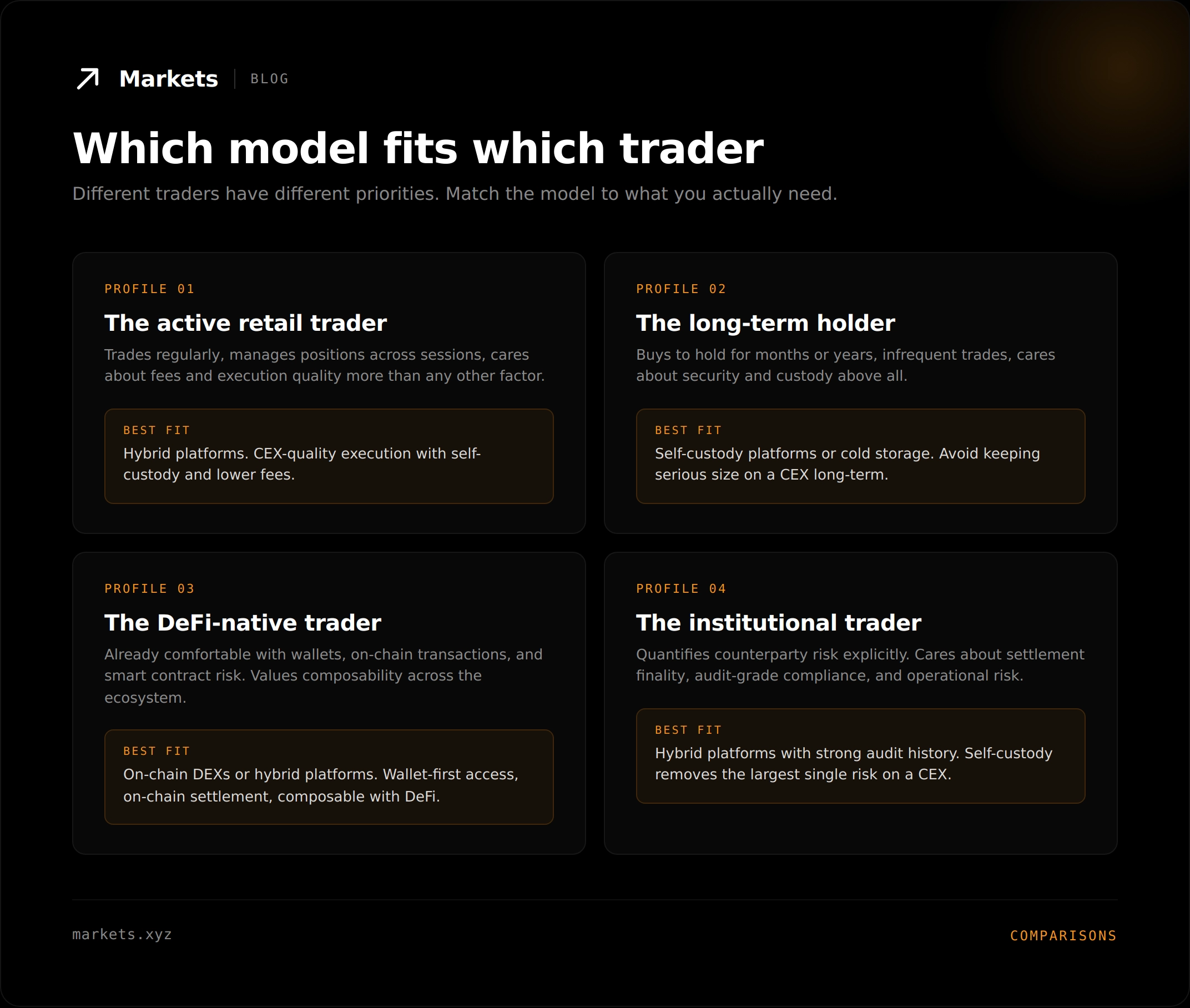

Which model fits which trader

Different traders have different priorities. The right model depends on what you're actually trying to do and how much each dimension of the comparison matters to your specific situation.

The active retail trader

Active retail traders trade regularly, manage positions across multiple sessions, and care about fees and execution quality more than any other single factor. The right fit is on-chain order-book infrastructure accessed through a strong trading terminal. Traders get fast execution, deep liquidity, advanced order types, wallet-based access, and lower all-in costs without going back to the custodial CEX model. For high-turnover traders, those savings compound across the trading year in a way that’s not marginal.

The long-term holder

Long-term holders buy to hold for months or years and trade infrequently. Their priority is security and custody. The right fit is self-custody. Cold storage wallets are the gold standard for serious size. For meaningful amounts on platforms, self-custody DEXs are the only model that doesn't leave the holder exposed to platform-level failure modes. Keeping serious long-term size on a CEX is taking a known risk for no real benefit.

The DeFi-native trader

DeFi-native traders are already comfortable with self-custody wallets, on-chain transactions, and smart contract risk. They value composability with the rest of the DeFi stack, on-chain settlement, and access to long-tail assets. The right fit is on-chain AMM DEXs for spot swaps and long-tail assets, or on-chain order-book infrastructure for active trading and perpetuals. Wallet-first access, on-chain settlement, and seamless integration with the broader DeFi ecosystem are structural to how this trader operates. A CEX doesn't fit the workflow.

The institutional trader

Institutional traders evaluate counterparty risk explicitly. They care about settlement finality, audit-grade compliance documentation, and operational risk. The right fit is mature on-chain order-book infrastructure with strong operational history, robust oracle design, clear risk controls, and interfaces that support professional workflows. Self-custody removes the largest single counterparty risk that exists on a CEX. On-chain settlement gives auditable finality. Strong platforms in this category increasingly meet the operational requirements institutions need, while delivering structural advantages CEXs cannot match.

How Markets.xyz delivers the structural advantages of both

Through Hyperliquid, Markets.xyz gives traders access to on-chain order-book execution, wallet-based access, and near-instant settlement. Through HIP-3, Markets can deploy and operate new perpetual markets across crypto, equities, indices, commodities, and FX. Through the terminal and mobile app, traders get a cleaner interface for accessing that infrastructure without having to think about the underlying stack.

Custody is self-custody by default. Funds remain in the user's wallet throughout the trade lifecycle. The contract has permission to execute trades and update positions, but it never takes possession of underlying balances. There is no centralized entity that can fail and take funds with it.

Asset coverage spans crypto perpetuals, equities like AAPL and TSLA, indices like US500, commodities like gold and oil, and FX pairs, all trading 24/7 through continuous oracle pricing from Kaiko. Access is open in 180+ countries, with no KYC required and no per-asset geographic gating. Trading fees are competitive with the leanest CEXs, with no spread tax, no withdrawal markup, and transparent funding rates.

The result is a product layer that captures the structural advantages of decentralized infrastructure and the execution quality previously associated only with centralized venues. Trade BTC, US500, or any other supported market through the same terminal, with wallet-based access, on-chain settlement, and 24/7 availability.

Self-custody, deep liquidity, 24/7 access, transparent execution. Start trading on markets.xyz.

The future: where the lines are blurring

The CEX vs DEX debate is becoming dated. The reasons to default to a CEX have narrowed to fiat on-ramps and regulatory familiarity. The reasons to default to a DEX have expanded to include execution quality, asset breadth, and 24/7 access across asset classes that used to be CEX-only. The technical gap that defined the choice for the first decade of crypto trading is closing fast.

What's not closing is the structural difference in custody and transparency. CEXs cannot eliminate their custodial risk. DEXs cannot introduce hidden execution that doesn't appear on-chain. These are architectural commitments, not feature choices. The trader who chooses a DEX is choosing a different relationship to the platform, not just a different feature set.

The next generation of trading products will look more modular: base trading infrastructure, oracle systems, market deployment layers, and user-facing terminals working together instead of everything living inside one centralized exchange. The category boundary between CEX and DEX will continue to blur. What will remain is the question of who holds your funds and whether the platform's execution can be independently verified. The answer to those two questions has not become less important as the technical gap has closed. If anything, it's become more important, because the trade-offs that used to make CEXs the practical choice have largely disappeared.

Frequently asked questions

The most common questions traders ask about decentralized vs centralized exchanges, answered directly.

Is one model objectively better than the other? Not universally. The right model depends on what the trader needs: fiat access, custody, execution quality, transparency, asset coverage, or trading workflow. Centralized exchanges still make sense for fiat on-ramps and account-based trading. AMM DEXs work well for DeFi-native spot swaps and long-tail assets. On-chain order-book infrastructure is increasingly the stronger model for active trading, especially when accessed through a trading terminal that combines fast execution, deep liquidity, wallet-based access, and on-chain settlement.

Are DEXs as fast as CEXs now? Modern order-book DEXs built on trading-specific chains match centralized exchange speed for nearly all practical purposes. Sub-second matching, deep order books, and atomic on-chain settlement are now standard on leading platforms. The first-generation AMM model was meaningfully slower. The current generation is not.

What happens to my funds during an exchange failure? On a centralized exchange, your funds are creditor claims in bankruptcy proceedings. Recovery depends on what assets the exchange actually controlled and how the legal process plays out. On a self-custody decentralized exchange, your funds remain in your own wallet. A platform failure does not affect your underlying balance. This is the single largest structural difference between the two models.

Do I need to know how to use a wallet to trade on a DEX? Yes. The learning curve for connecting a wallet is genuinely small, but it is a step beyond the email-and-password experience of a centralized exchange. Most modern wallets like MetaMask, Rabby, or hardware wallets make the experience straightforward, and platforms like Markets.xyz have streamlined onboarding to minimize the friction.

Are DEX fees actually lower than CEX fees? On a per-side basis, yes, for most active trading. Modern DEX trading fees in the 0.02 to 0.05% range are lower than the 0.05 to 0.20% typical on CEXs. Plus, there's no withdrawal markup, no spread tax on quoted prices, and no hidden fee structure. The all-in cost difference compounds meaningfully across active trading.

Why don't all DEXs offer non-crypto assets like stocks and indices? Because trading non-crypto assets requires reliable oracle infrastructure to bring external prices on-chain. Most DEXs are not built with this infrastructure. Platforms like Markets.xyz use Kaiko oracles specifically to enable 24/7 trading of equities, indices, FX, and commodities through smart contracts. This is the structural step that turned DEXs from crypto-only venues into full multi-asset trading platforms.

Will regulators shut down decentralized exchanges? Regulatory pressure exists on the front-end interfaces that DEXs use. The underlying smart contracts cannot be shut down by any single party. Compliance-oriented platforms apply regional restrictions on their front ends to satisfy local regulations. The protocols themselves remain accessible. This is one of the reasons the model has structural resilience that centralized exchanges cannot match.

Conclusion

Custody, fees, access. That's the real difference. Centralized exchanges hold your funds, set their fees with hidden costs, and gate access by jurisdiction. Decentralized exchanges leave funds in your wallet, settle on-chain with transparent fees, and accept any wallet that connects. The technical gaps that used to make CEXs the default for active trading have largely closed. The structural differences that define the choice are more important now than they were three years ago, not less.

On-chain order-book infrastructure and trading terminals like Markets.xyz represent where the market is heading. CEX-quality execution. Wallet-based access. On-chain settlement. Continuous 24/7 access across crypto, equities, indices, FX, and commodities. The trade-offs that used to define the DEX vs CEX choice are narrowing. The structural advantages of decentralized infrastructure remain.

The trader's job is to evaluate their own priorities and choose the model that fits. For long-term holders, self-custody is the right answer. For active traders, on-chain order-book infrastructure accessed through a strong trading terminal is the right answer. For DeFi-native users, AMM DEXs or on-chain order-book systems fit depending on the trade. For institutions, mature decentralized trading infrastructure with strong risk controls is the right answer. The remaining cases where a pure CEX is the best choice are increasingly narrow. The infrastructure has caught up. The choice is no longer convenience vs principles. It's outdated infrastructure vs current infrastructure.

Trade on infrastructure designed for the next era of markets. Start trading on markets.xyz.

Risk disclaimer: Trading involves substantial risk, including the possible loss of principal. Both centralized and decentralized exchanges carry distinct risks, including counterparty risk on centralized platforms and smart contract risk on decentralized platforms. Leverage amplifies both gains and losses. Past performance is not indicative of future results. Markets.xyz is not available to residents of the United States, the United Kingdom, or the province of Ontario in Canada. Full terms, conditions, and risk disclosures are available at markets.xyz. Information in this article is for educational purposes only and does not constitute financial, investment, or trading advice.