NVIDIA earnings preview: Blackwell, China, and the next test for the AI trade

NVIDIA reports Q1 fiscal 2027 earnings this week. What to watch in NVDA: Blackwell demand, China H200 chips, margins, and Q2 guidance.

NVIDIA’s April-quarter report is not just a check on AI demand. Investors need proof that Blackwell is ramping cleanly, margins are holding, China H200 approvals can convert into shipments, and customers can deploy the power and infrastructure needed for the next leg of the AI buildout.

NVIDIA reports its April-quarter results, officially Q1 fiscal 2027, after the U.S. market close on Wednesday, May 20. NVIDIA has also said it will release written CFO commentary alongside results and host its earnings call at 2:00 p.m. PT / 5:00 p.m. ET.

This is one of the most important earnings reports of the quarter because it is carrying far more than company-specific risk. NVIDIA sits at the center of the AI infrastructure trade, and this report lands just as investors are trying to decide whether the next leg of AI spending still belongs to GPUs alone or to a broader stack that now includes networking, optics, memory, power conversion, cooling, and grid-connected deployment. Business Insider’s market preview captured that tension well: Big Tech’s recent earnings largely confirmed AI spending appetite, but investors remain focused on capex intensity and how quickly those investments translate into returns.

NVIDIA is entering the print with little ambiguity around the baseline. In its fiscal 2026 fourth-quarter release, the company reported $68.1 billion of quarterly revenue, $62.3 billion of Data Center revenue, and $215.9 billion of full-year revenue. For Q1 fiscal 2027, management guided to $78.0 billion of revenue, plus or minus 2%, with non-GAAP gross margin at 75.0%, plus or minus 50 basis points, and non-GAAP operating expenses around $7.5 billion. The company also flagged an accounting change that matters for comparability: beginning in Q1 fiscal 2027, NVIDIA’s non-GAAP measures will include stock-based compensation expense.

At the same time, the stock is no longer set up like an under-owned compounder that can rally on a merely respectable beat. The latest market data showed NVDA at roughly $222 with a market cap of about $5.44 trillion, while recent sessions saw the stock trade as high as $236.54 and close near $225.83 at a fresh record before pulling back. Framed simply, the market is already pricing NVIDIA as the central beneficiary of the AI buildout. The open question is whether the company can keep lifting the bar from here.

Consensus snapshot

Metric | Company guide | Visible Alpha consensus | FactSet consensus | Why it matters |

|---|---|---|---|---|

Q1 revenue | $78.0B ± 2% | $78.5B | $78.85B | Consensus is already near the upper half of guidance |

Q1 EPS | Not guided | n/a | $1.75 | Profitability is less important than guide quality, but still a benchmark |

Q1 non-GAAP gross margin | 75.0% ± 50 bps | n/a | n/a | Cleanest read on Blackwell economics and mix |

Q1 non-GAAP operating expenses | ~$7.5B | n/a | n/a | Matters more because stock comp is now included in non-GAAP |

Q1 Data Center revenue | Not guided | $72.8B | n/a | The single most important reported number |

Q2 revenue expectation | To be guided | n/a | $87.09B | The real event for the stock |

Earnings implied move | n/a | n/a | ~5.8% options-implied | Shows how much movement the market is pricing |

Source note: company guidance comes from NVIDIA’s fiscal Q4 2026 release; Visible Alpha figures are from S&P Global’s preview; FactSet figures are cited by Investor’s Business Daily; the options-implied move comes from Bloomberg options data cited by Investing.com.

Data Center revenue is still the number that matters most. NVIDIA’s Data Center business reported $62.3 billion in Q4 fiscal 2026, up 22% sequentially and 75% year over year, and full-year Data Center revenue reached $193.7 billion. Visible Alpha’s Q1 fiscal 2027 consensus now sits at roughly $72.8 billion, but just as important as the number is the dispersion around it: S&P Global says analyst estimates for quarterly Data Center revenue range from $65.4 billion to $78.0 billion, which tells you the Street still does not have a settled view on the true speed of the Blackwell ramp.

That uncertainty is even clearer in the underlying Blackwell assumptions. S&P Global’s Visible Alpha preview says B-series revenue estimates for Q1 range from $9.0 billion to $67.0 billion, with consensus around $34.6 billion. That is an unusually wide spread for a company this closely covered. For investors, the implication is clear: a headline revenue beat will matter, but commentary on Blackwell supply, deployment timing, and system mix will matter more because those are the variables the market still cannot pin down with confidence.

Q2 guidance is the real event. FactSet figures cited by Investor’s Business Daily put the Street at roughly $87.09 billion of revenue and $1.95 of EPS for the current quarter, and some analysts cited there suggest that a guide above $90 billion would be reassuring, even if not strictly necessary. That is the framework that should shape expectations into the print. NVIDIA can clear Q1 and still struggle if the Q2 guide does not signal another step up in the AI spending cycle.

This is one reason the stock reaction is often harder than the headline numbers suggest. Bloomberg options data cited by Investing.com implies a roughly 5.8% move around the report, which is large in absolute terms but not especially forgiving for a company whose valuation already embeds leadership in AI infrastructure. Put differently, investors are not paying for a decent quarter. They are paying for another beat-and-raise cycle.

Gross margin will decide the quality of the quarter. NVIDIA guided non-GAAP gross margin to 75.0%, plus or minus 50 basis points, and said that figure already includes roughly 0.1 percentage point of impact from stock-based compensation. That is a strong starting point, especially because fiscal 2026 gross margin was pulled down by both the transition from Hopper HGX systems to Blackwell full-scale data center solutions and a $4.5 billion H20 excess-inventory and purchase-obligation charge in the first quarter of fiscal 2026.

The reason margin matters so much is that it is where several moving pieces meet. Blackwell full-system mix, memory costs, networking attach rates, and any future China revenue structure all run through gross margin. S&P Global notes that the Visible Alpha consensus for fiscal 2027 Data Center gross margin is about 76.3%, down from roughly 78% in fiscal 2024 and fiscal 2025. That does not break the thesis, but it does raise the standard for the call: investors need comfort that NVIDIA is not simply growing fast, but that it is still growing well.

China is the swing factor, but it is not yet a revenue line. NVIDIA’s own Q1 guide assumes no Data Center compute revenue from China, which made sense at the time it was issued. Since then, Reuters has reported that the U.S. cleared roughly 10 Chinese companies to buy H200 chips, including Alibaba, Tencent, ByteDance, and JD.com, with approved purchasers reportedly able to buy up to 75,000 chips each. Reuters also reported that approved distributors include Lenovo and Foxconn.

The important nuance is that no deliveries had taken place when Reuters published that report. The same reporting said Chinese firms had pulled back after guidance from Beijing, that China remains wary of deepening dependence on U.S. suppliers, and that the route to completed sales has become unusually complex. Reuters also said one feature of the arrangement would direct 25% of revenue from those sales to the U.S. government and require the chips to transit U.S. territory before onward shipment, which means convertibility, economics, and execution all remain open questions.

That ambiguity persists. On May 18, Reuters reported that Jensen Huang said he believes China’s market will open over time, but also that NVIDIA has received U.S. licenses without having yet secured the necessary Chinese approval. A day earlier, Reuters reported that U.S. Trade Representative Jamieson Greer said chip export controls were not a major topic in the recent bilateral discussions, implying that a near-term breakthrough on H200 exports remains distant. The correct way to frame China into earnings is therefore not as “reopened,” but as potential upside that has not yet converted into recognized revenue.

Power and deployment bottlenecks are the next-order risk. The AI trade is no longer just about who sells the accelerators. It is increasingly about who can commission the underlying factories. NVIDIA’s own recent releases point in that direction. Its DSX AI Factory blueprint now includes contributions from Eaton, Schneider Electric, Siemens, Vertiv, Jacobs, Trane and others, while NVIDIA says energy leaders including GE Vernova, Hitachi, Siemens Energy and Emerald AI are using the reference architecture to help unlock grid capacity for new AI factories. A separate NVIDIA-IREN announcement said the two companies intend to support deployment of up to 5 gigawatts of DSX-aligned AI infrastructure over time.

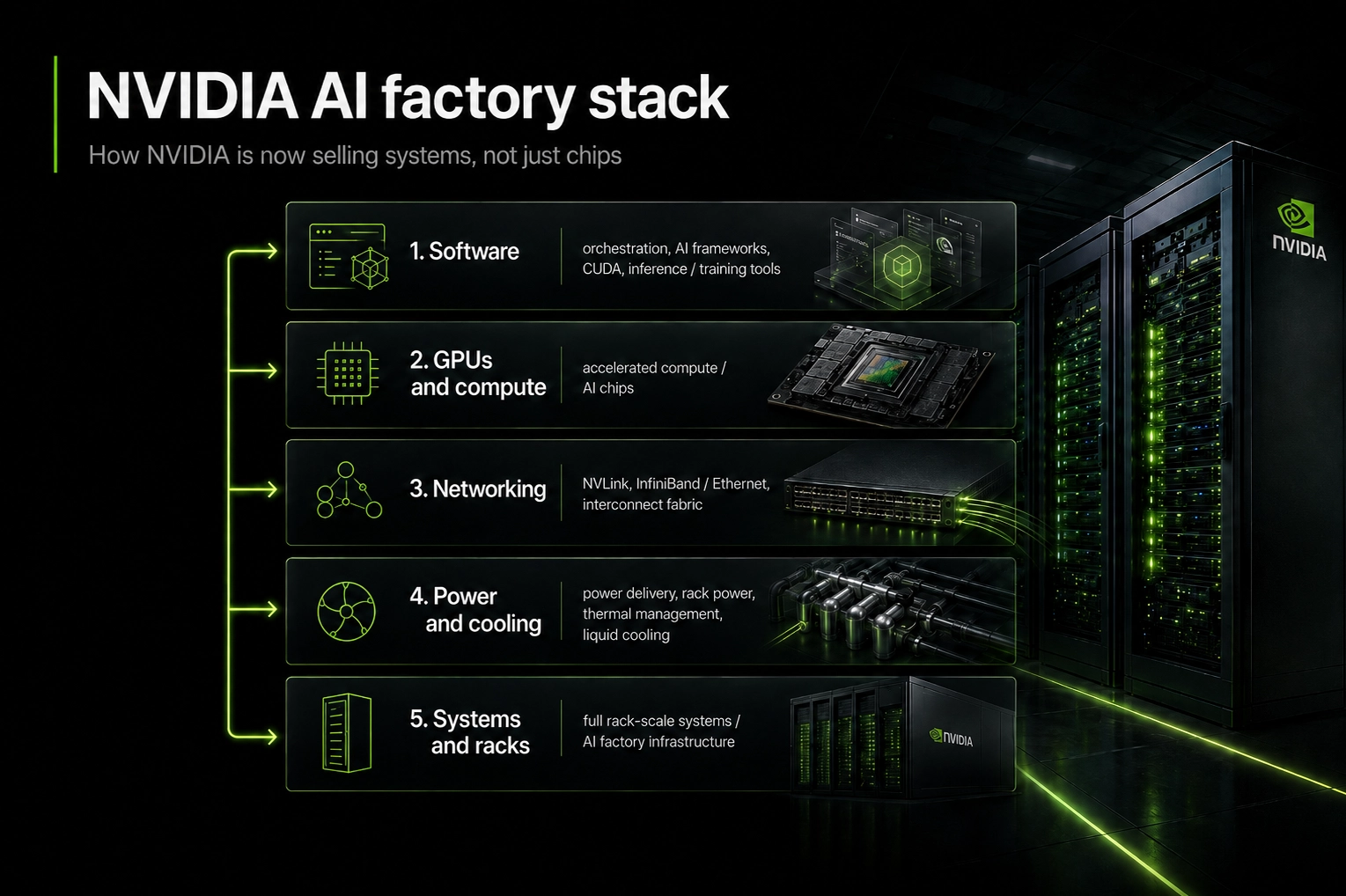

NVIDIA’s own filings also show that the mix inside the Data Center business is getting broader and more system-like. In the fiscal 2026 Form 10-K, the company said Data Center networking revenue grew 142% year over year, driven by NVLink compute fabric for GB200 and GB300 systems and by Ethernet and InfiniBand platforms. That matters because it reinforces the idea that NVIDIA is selling more of the AI factory stack, not just the GPU die. It also means the bottleneck can migrate out of chip availability and into system-level deployment.

The attached semis memo is useful here because it visualizes the engineering shift behind the market narrative. The diagrams on pages 5, 6, and 10 show the transition from more traditional power architectures toward 800V HVDC-style approaches and sharply higher rack power density, with the stack moving from conventional low-density configurations toward hundreds of kilowatts per rack. That framing supports a simple but important inference: even if NVIDIA remains demand-constrained at the chip level, revenue conversion can become gated by power availability, cooling, interconnect, and commissioning speed at the rack and campus level.

This is why the report matters beyond NVIDIA. Business Insider’s market preview argued that the AI trade is at a crossroads after a month in which AI-heavy areas of Big Tech largely beat, yet investors stayed fixated on capex intensity and the pace of the payoff. At the same time, Wall Street positioning remains aggressive. Business Insider reported that Bank of America recently lifted its target price to $320 and Wells Fargo to $315, with BofA describing NVIDIA as a top sector pick and arguing the AI data-center market could reach $1.7 trillion by 2030. That does not tell you where the stock must trade next week, but it does tell you expectations remain elevated on both fundamentals and narrative.

There is also a longer-horizon frame investors will be listening for. Reuters reported from GTC in March that Jensen Huang said the revenue opportunity for Blackwell and Rubin by the end of 2027 was likely to be more than $1 trillion, excluding networking and certain newer processor lines. Business Insider later noted that investors are now watching whether NVIDIA reiterates or refines that multi-year framework. This matters because the stock is not being valued as a one-quarter story. It is being valued as the dominant supplier to a multi-year AI infrastructure buildout.

Scenario analysis

The scenario framework below is an inference based on management guidance, recent consensus estimates, options pricing, and the latest China reporting.

Scenario | What it looks like | What the market is likely to hear | Likely read-through |

|---|---|---|---|

Bull case | Revenue at or above the high end of guidance, Data Center ahead of Visible Alpha, gross margin at or above 75%, Q2 guide clearly above Street expectations, constructive Blackwell and China commentary | Blackwell is scaling, margins are holding, China is becoming additive, and deployments are not bottlenecked enough to derail the next leg | Reinforces the AI infrastructure thesis for NVIDIA and for the wider semi and infrastructure complex |

Base case | Revenue around consensus, gross margin in range, Q2 guide roughly in line with current Street numbers, China still unresolved | Core demand is intact, but the company is not obviously re-accelerating beyond what the stock already discounts | Mixed reaction, especially if the market wanted a cleaner beat-and-raise |

Bear case | Revenue only modestly above guide or below high-end expectations, gross margin softens, Q2 guide disappoints relative to bullish whispers, China remains stalled, or deployment commentary points to friction | The business is still strong, but the market may conclude the phase of constant upside surprise is becoming harder | Downside risk remains meaningful because the valuation already assumes leadership persists |

Positioning for long-term investors. The long-term case still rests on NVIDIA remaining the system-level winner in AI infrastructure. If Data Center growth stays strong, gross margin remains healthy, and management can guide Q2 without blinking, short-term volatility is less important than confirmation that the company is still absorbing more of the stack over time. The most useful question for long-only holders is not whether Q1 beats by a small amount, but whether the report keeps the multi-quarter Blackwell and Rubin trajectory intact.

Positioning for traders. This is a high-expectation, high-volatility setup. Consensus is already near the upper end of the guided range, options are pricing a material move, analyst targets have moved higher, and China headlines have added upside optionality on top of an already crowded AI leadership trade. In that kind of setup, “good” and “good enough” are not the same thing.

Positioning for investors without a position. Waiting for confirmation is a perfectly rational stance. If the goal is to own the durable part of the thesis rather than guess the next 24 hours of price action, the highest-value information from this report will be the Q2 guide, the cadence of Blackwell deployment, the treatment of China in management commentary, and whether NVIDIA sounds confident that customers can deploy capacity quickly enough to match demand.

The cleanest takeaway into the print is this: NVIDIA still looks like the strongest company in the AI infrastructure trade, but the stock now needs more than a solid quarter. It needs a quarter that confirms the market’s most demanding assumptions. If management can show strong Data Center revenue, a convincing Q2 guide, stable gross margin, credible China optionality, and no meaningful signal that power and deployment are turning into an execution bottleneck, the thesis likely survives just fine. If one or more of those pillars wobbles, the market’s response may be harsher than the absolute numbers alone would suggest.

We will track NVIDIA’s results live in our Markets app. Download it to get the full breakdown as soon as the numbers hit.

https://markets.xyz/mobile-app

NVIDIA perpetual futures are also accessible from the web app

https://markets.xyz/trade/xyz:NVDA

FAQ

Where can I trade NVDA during earnings?

Eligible users can trade NVDA during earnings on Markets, either through the web app at markets.xyz or through the Markets mobile app, the web-based mobile version available at markets.xyz/mobile-app.

This means you can follow the earnings release, after-hours reaction, guidance, and market repricing from one place instead of waiting for the next regular market session. Earnings events can be highly volatile, so traders should always check liquidity, oracle price, funding, leverage, and liquidation risk before opening a position.

When does NVIDIA report earnings?

NVIDIA reports Q1 fiscal 2027 earnings on Wednesday, May 20, 2026, after the U.S. market close. The company’s earnings call is scheduled for 2:00 p.m. PT / 5:00 p.m. ET, and the quarter being reported is the one that ended April 26, 2026.

What are Wall Street analysts expecting?

Management guided Q1 revenue to $78.0 billion, plus or minus 2%, with non-GAAP gross margin near 75.0%. Visible Alpha, as cited by S&P Global, expects roughly $78.5 billion of total revenue and $72.8 billion of Data Center revenue, while FactSet estimates cited by Investor’s Business Daily put total revenue near $78.85 billion and EPS near $1.75.

What is the most important number in the report?

Reported Data Center revenue is the most important realized metric, but Q2 guidance is likely to matter more for the stock. Investors are trying to determine whether Blackwell demand, margins, and deployment visibility still justify a premium multiple at a market cap above $5 trillion.

Why does China matter this quarter?

China matters because NVIDIA’s Q1 guide assumed no Data Center compute revenue from China, yet Reuters subsequently reported that the U.S. cleared roughly 10 Chinese firms to buy H200 chips even though no deliveries had started and Chinese approval was still pending. That makes China a real upside option, but not yet a booked revenue stream.

Why are power and infrastructure bottlenecks relevant to NVIDIA?

NVIDIA is increasingly selling rack-scale AI systems, not just individual chips. The company’s DSX blueprint now includes power, cooling, and facilities partners, and its IREN partnership is aimed at multi-gigawatt AI infrastructure deployment. The attached semis memo also shows how AI rack density and power architecture are shifting toward much higher-intensity configurations, which means revenue can be constrained by deployment readiness even when end demand stays strong.