Understanding smart contract trading

Learn how smart contract trading works. Mechanics, advantages, and risks of executing trades on-chain through programmable code instead of intermediaries.

Introduction

Consider what happens when you place a trade on a traditional exchange. You deposit funds into the exchange's custody. You submit an order to the exchange's matching engine. The exchange decides whether to fill it, at what price, and in what order. The trade settles on the exchange's internal ledger. If you want to withdraw, you wait for the exchange to approve it. At every step, a single company holds your money, controls execution, and decides who can do what. You trust the exchange. Implicitly, you have no choice.

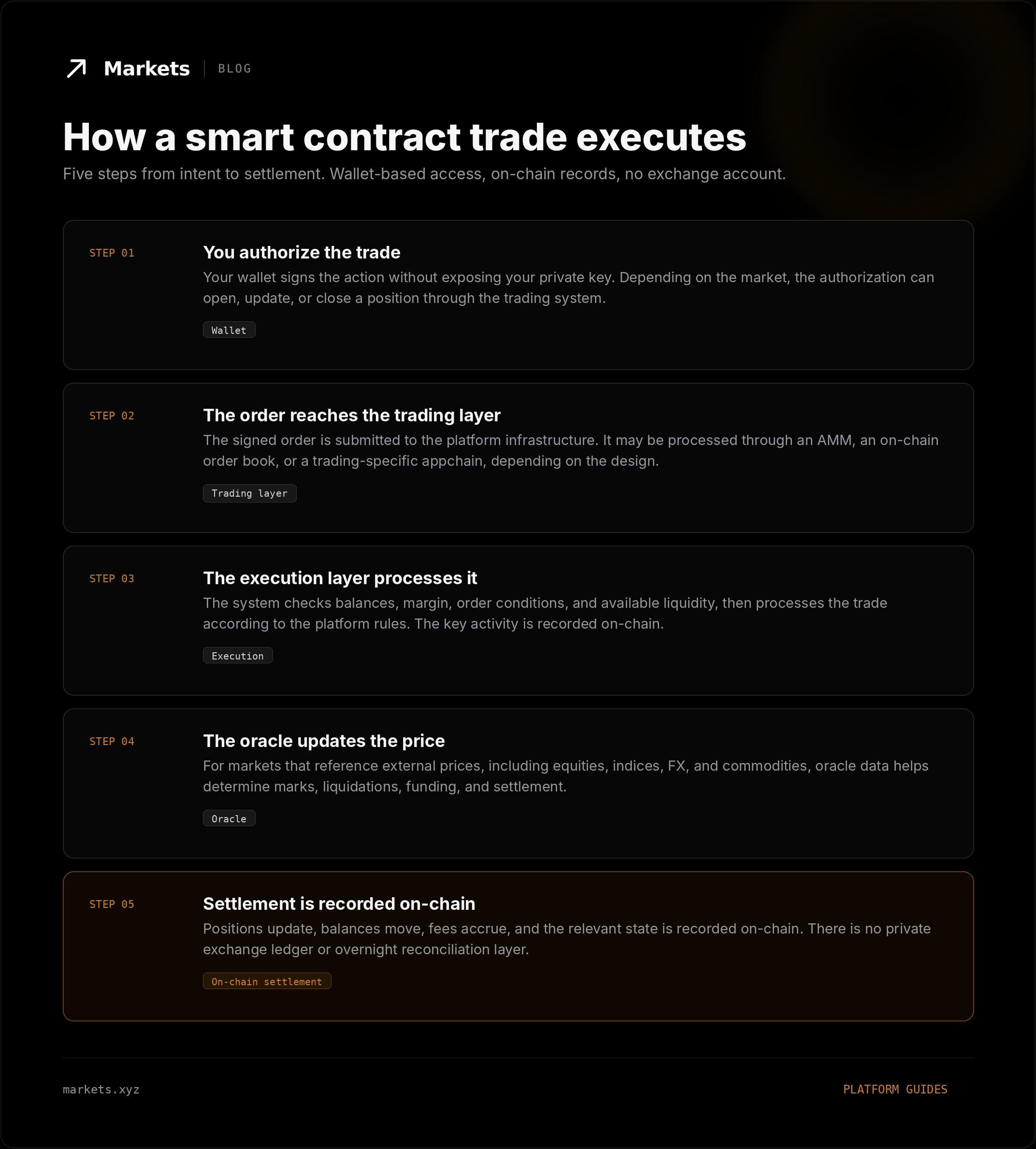

Now consider the same trade on an on-chain trading platform. You connect your wallet, authorize the trade, and interact with trading infrastructure that records the key parts of the lifecycle on-chain. Depending on the design, execution may happen through AMM pools, on-chain order books, or trading-specific appchains. The important difference is that the platform does not operate like a traditional exchange account. Access is wallet-based, settlement is recorded on-chain, and the trading system leaves a public record that can be independently inspected.

This isn’t just a technical change. It’s a structural one. On-chain trading moves custody, settlement, and core trading activity away from a private exchange-controlled database and toward blockchain-based infrastructure. The implications touch every part of the trading experience, from how positions are settled to who can access the platform to what happens during volatility.

This guide explains how smart contract trading actually works. We’ll cover how trades flow through on-chain infrastructure, how smart contract platforms differ from centralized exchanges, the core components that make up an on-chain trading venue, how orders get matched and settled, the role of oracles, the specific risks of trading on-chain, why this architecture enables 24/7 markets, and how Markets.xyz combines a trading terminal, mobile app, and HIP-3 deployer on top of Hyperliquid infrastructure.

What is a smart contract and how does it execute a trade?

Before getting into trade execution specifically, it helps to understand what a smart contract is and what makes on-chain trading infrastructure different from a centralized exchange.

The basics of smart contracts

A smart contract is a program that runs on a blockchain. It has its own address, can hold balances, can receive and send transactions, and executes according to predefined rules. In simple terms, it is software that updates blockchain state when specific conditions are met.

That does not mean every smart contract trading system is fully open source, and it does not mean every line of infrastructure code is visible. The important distinction is that on-chain trading systems expose far more of the system’s state and activity than centralized exchanges do. Balances, positions, fills, fees, liquidations, and settlement can leave a public record that traders and observers can inspect directly.

This is the foundational difference from a centralized exchange. The matching engine of a centralized exchange is a proprietary system whose behavior you can only infer. A smart contract trading platform gives traders a system where the key trading activity is recorded on-chain, making the platform more verifiable than a private exchange database.

How a trade actually flows through a smart contract

A smart contract trade is not one universal process. Different platforms use different architectures. Some trades execute against AMM pools. Some execute through on-chain order books. Some use trading-specific appchains where matching, positions, and settlement are handled by infrastructure designed specifically for financial markets.

The user experience is simpler than the architecture behind it. You connect your wallet, authorize the trade, and interact with trading infrastructure that records the key parts of the lifecycle on-chain. The order is processed by the platform’s execution layer. The position updates according to the platform’s rules. Settlement is recorded on-chain.

This is the opposite of how a centralized exchange works internally. In a centralized exchange, order intake, matching, custody, price discovery, and settlement all happen inside one private system. The user trusts that the system works correctly. With on-chain trading infrastructure, the user can inspect the system’s state and activity instead of relying only on an exchange-controlled ledger.

What "on-chain" really means in practice

On-chain means recorded on the blockchain. In trading systems, the key state changes, such as fills, positions, balances, fees, liquidations, and settlement, are recorded in a way that is tamper-resistant and publicly inspectable. The blockchain becomes the source of truth for the trading system, rather than a private database controlled by a centralized exchange.

This has practical consequences for traders. Settlement does not depend on an exchange’s internal reconciliation process. There is no T+2 window like in traditional finance. There is no private ledger that can disagree with the public settlement layer. Once the relevant transaction or state update is finalized by the chain, the trading system reflects that state.

The result is not “no trust.” Traders still need to evaluate the chain, the oracle design, the market structure, the liquidation engine, and the platform’s implementation. But the trust model is different. Instead of trusting a company’s private database, traders can verify much more of the trading system’s state directly.

Smart contract trading vs centralized exchange trading

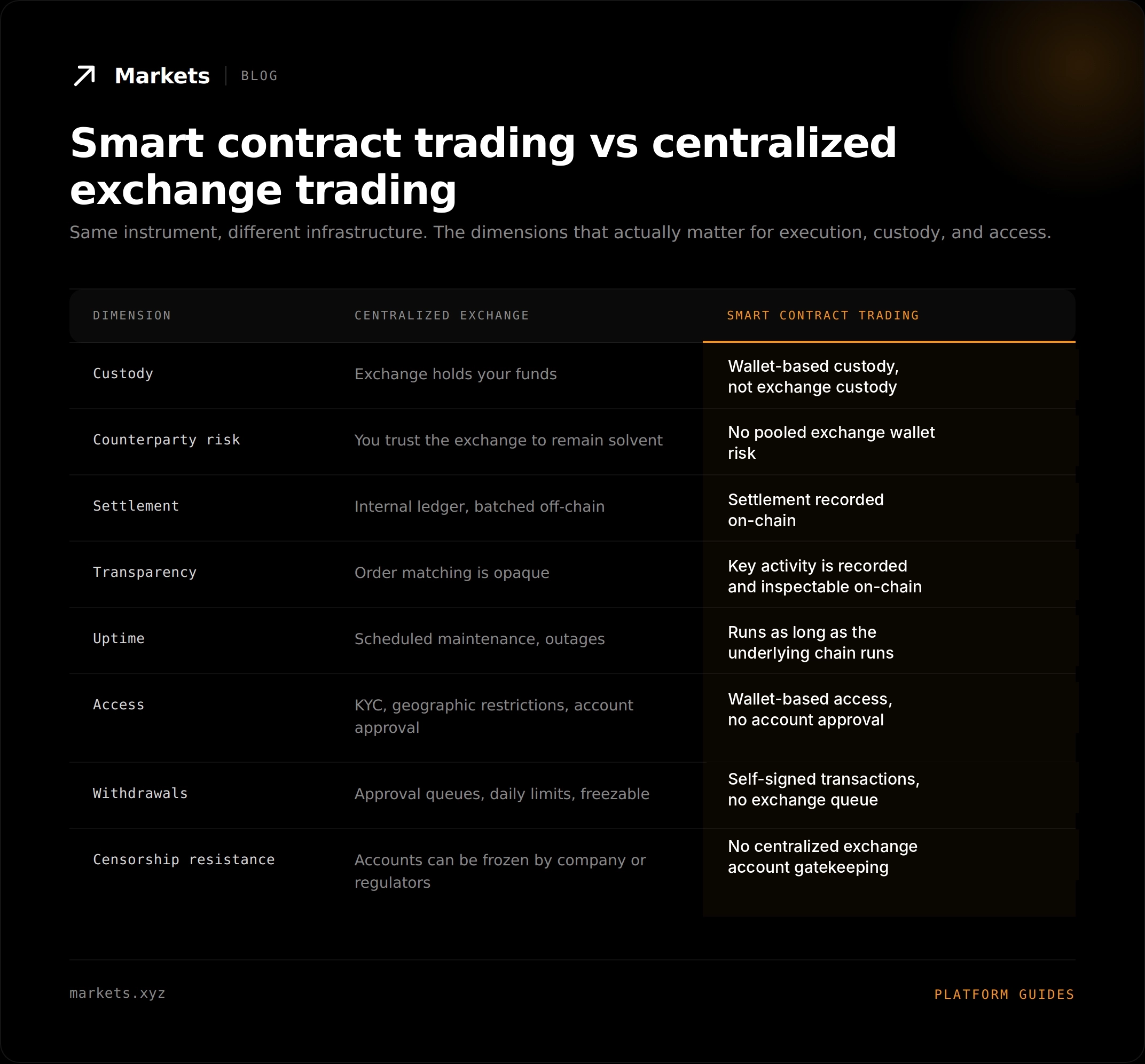

Both kinds of platforms let you trade. The instruments can look the same on the surface. But the underlying infrastructure produces meaningfully different outcomes across custody, settlement, transparency, access, and every dimension that matters for serious traders.

Custody and counterparty risk

On a centralized exchange, you deposit funds into the exchange’s wallets. From a legal and operational standpoint, those funds become part of the exchange-controlled system while they are on the platform. If the exchange becomes insolvent, gets hacked, or is shut down by regulators, your access depends on the exchange’s bankruptcy, recovery, or withdrawal process. History across multiple major exchange failures shows this can range from full recovery to total loss.

On a smart contract trading platform, custody is self-custodial rather than exchange-custodial. Users do not deposit assets into a centralized exchange account or rely on an exchange operator to process withdrawals. Depending on the protocol, collateral may be posted to smart contracts or trading accounts, but the custody model is still structurally different from a CEX: access is controlled by the user’s wallet, settlement is on-chain, and there is no pooled exchange wallet standing between the trader and the system.

Execution and settlement mechanics

Centralized exchanges run their order matching off-chain on internal servers. Trades settle on the exchange’s internal ledger, with reconciliation happening in the background. Withdrawals to your own wallet require the exchange to broadcast a transaction, which can take minutes or hours and is subject to approval queues.

Smart contract trading platforms use blockchain infrastructure for settlement and state updates. Depending on the architecture, matching may happen through AMM pools, on-chain order books, or trading-specific appchains. The important distinction is that settlement is recorded on-chain rather than only inside an exchange-controlled database. Once the relevant state update is finalized, the trading system reflects the settled position without relying on an internal reconciliation process controlled by a single company.

Transparency and verifiability

On a centralized exchange, you take it on faith that the matching engine treats your orders fairly. You can’t verify whether the exchange is frontrunning your trades, whether market makers get preferential treatment, or whether the order book you see matches the order book the matching engine actually uses. The system is a black box. The exchange’s incentives and your incentives are not always aligned, and you have no way to check.

Smart contract trading is far more verifiable than centralized exchange trading. The key trading activity, including orders, fills, positions, fees, liquidations, balances, and settlement, can be recorded on-chain and inspected directly. That does not mean every part of every platform is fully open source, and it does not mean there is no trust involved. It means the most important parts of the trading lifecycle leave a public record. The trust model changes from “believe the exchange” to “verify the system’s state and activity.”

Censorship resistance and access control

Centralized exchanges control access. They require KYC, restrict by country, freeze accounts at their discretion, and comply with whatever regulatory orders apply. From the exchange’s perspective, this is necessary. From the trader’s perspective, it means access can be revoked at any time, for reasons that may have nothing to do with the trader’s own behavior.

Smart contract trading platforms operate closer to the protocol level. Access is wallet-based rather than account-based, and users do not go through the same KYC and account approval process that defines centralized exchanges. Front-end interfaces may apply geographic restrictions for compliance reasons, and specific systems can still include protocol-level controls, but the access model is structurally different from a centralized company deciding who can open, keep, or withdraw from an account.

Trade through on-chain infrastructure, not exchange-controlled accounts. Wallet-based access, transparent settlement, and continuous markets. Start trading on markets.xyz.

The components of a smart contract trading platform

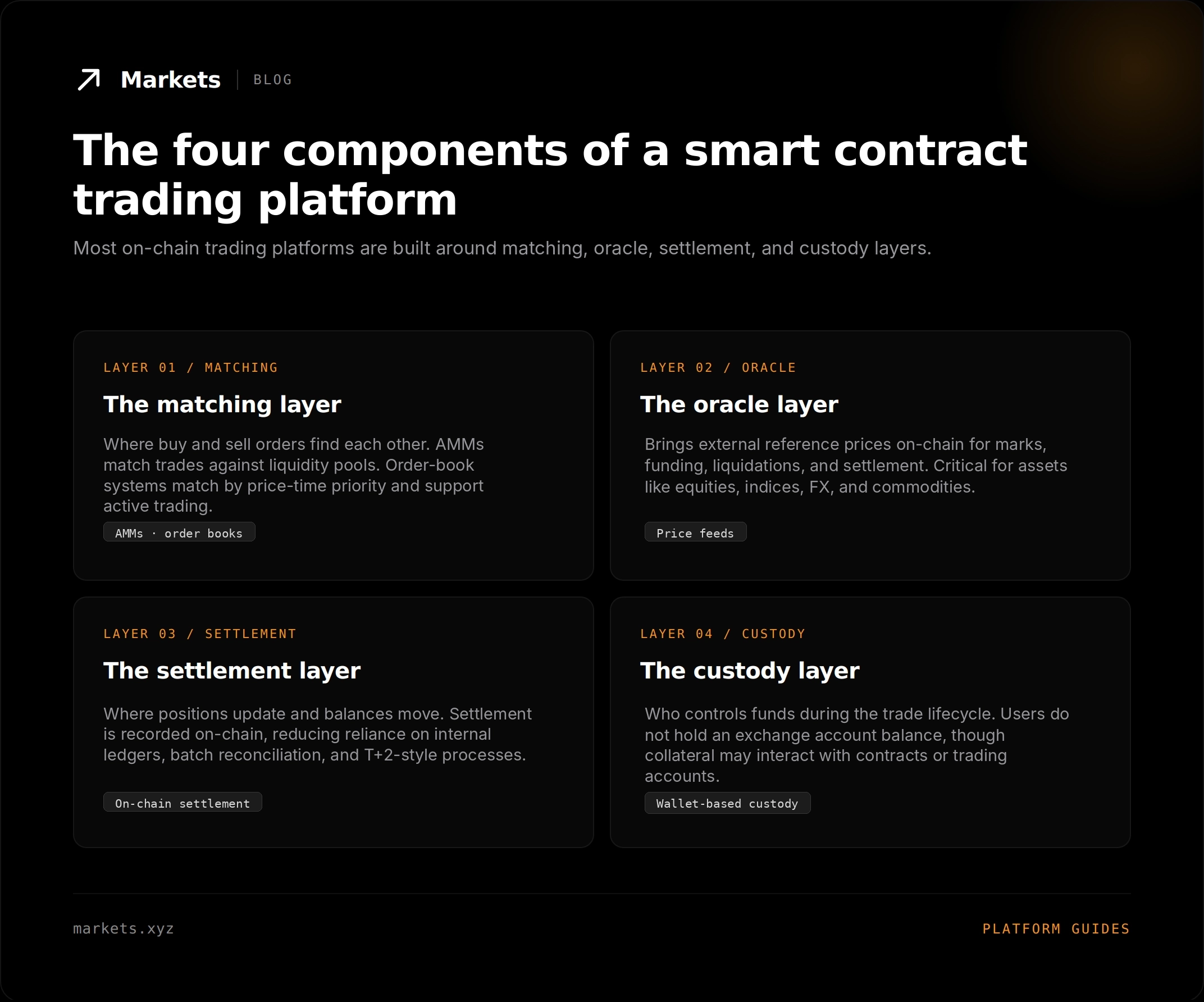

Every smart contract trading platform is built from the same four components. Each one is responsible for a different part of the trade lifecycle. The quality of each layer determines the quality of the platform. Understanding these components is how you evaluate any platform that claims to be a serious smart contract trading venue.

The matching layer

The matching layer is where buy and sell orders find each other. There are two major models. AMMs, or automated market makers, match trades against liquidity pools using mathematical curves. Order-book systems match individual buy and sell orders by price-time priority, closer to how traditional exchanges work.

For active trading, order books are generally preferred. They support limit orders, conditional orders, tight spreads, and professional market makers. AMMs remain important for DeFi-native spot swaps and long-tail assets, but they are usually less efficient for high-turnover, leveraged, or professional trading.

The oracle layer

Smart contracts only know what’s on-chain. For trading assets whose reference price comes from outside the chain, including equities, indices, commodities, FX, and crypto prices from other venues, the platform needs an oracle to bring that price data on-chain. The oracle layer is responsible for publishing reliable price feeds that the trading system can use for marks, funding, liquidations, and settlement.

Oracle quality matters enormously. A bad oracle can be manipulated, can lag real prices, or can fail during volatility. Good oracle systems use multiple data sources, deviation checks, fallback logic, and aggregation methods designed to reduce manipulation risk. For non-crypto assets traded 24/7, the oracle layer is especially important because the platform needs defensible pricing even when the underlying traditional market is closed.

The settlement layer

The settlement layer is where positions update and balances move. On smart contract platforms, settlement happens on-chain at the moment the trade executes. There is no separate batch process, no overnight reconciliation, no T+2 window. The blockchain itself is the source of truth, and once a transaction is finalized, the trade is settled.

Settlement speed depends on the underlying chain. Some chains finalize in seconds. Some take minutes. For active trading, faster finality means less exposure to chain-level risks and a better user experience. This is one of the reasons trading-specific chains like Hyperliquid have emerged. General purpose chains were not built for the throughput trading requires.

The custody layer

The custody layer determines who controls funds during the trade lifecycle. In self-custodial trading systems, users do not hold an exchange account balance managed by a centralized company. Depending on the design, collateral may be posted to smart contracts or protocol-level trading accounts, but withdrawals and access are not controlled by a centralized exchange operator. This is one of the most important structural differences between smart contract trading and centralized exchange trading.

Self-custody reduces platform-level counterparty risk. The risks that remain are smart contract risk, oracle risk, user key management, and chain-level risk, not company solvency or an exchange operator refusing withdrawals.

How orders get matched and settled on-chain

Different smart contract platforms use different matching architectures. The choice has consequences for capital efficiency, slippage, fees, and the kinds of strategies that work well on the platform.

Order book-based execution

Order book platforms maintain a list of buy and sell orders at different price levels. When a new order comes in, it's matched against the existing book by price-time priority. Limit orders that don't match immediately stay on the book until they fill or get canceled. Market orders fill against the best available prices on the book.

Order books are familiar to anyone who has traded on a traditional venue. They support tight spreads, professional market makers, limit and stop orders, and the full range of strategies that work in traditional markets. The challenge has historically been doing this on-chain at the speed and throughput that active trading requires.

AMM-based execution

AMMs replace the order book with a liquidity pool. Traders interact with the pool, and a mathematical formula determines the price based on the current state of the pool's reserves. Liquidity providers deposit assets into the pool and earn fees in return. There are no individual buy and sell orders, just pool interactions.

AMMs are simpler to implement on-chain and work well for long-tail assets that wouldn't have deep order books. They're less efficient for active trading because every trade moves the price along the curve, leading to more slippage on large orders than an order book with deep liquidity would produce. For most professional trading, order books are still the preferred architecture.

Trading-specific order-book infrastructure

A newer category is trading-specific order-book infrastructure. Instead of trying to make an AMM behave like an exchange, these systems rebuild the exchange stack around order books, professional market makers, fast finality, and on-chain settlement.

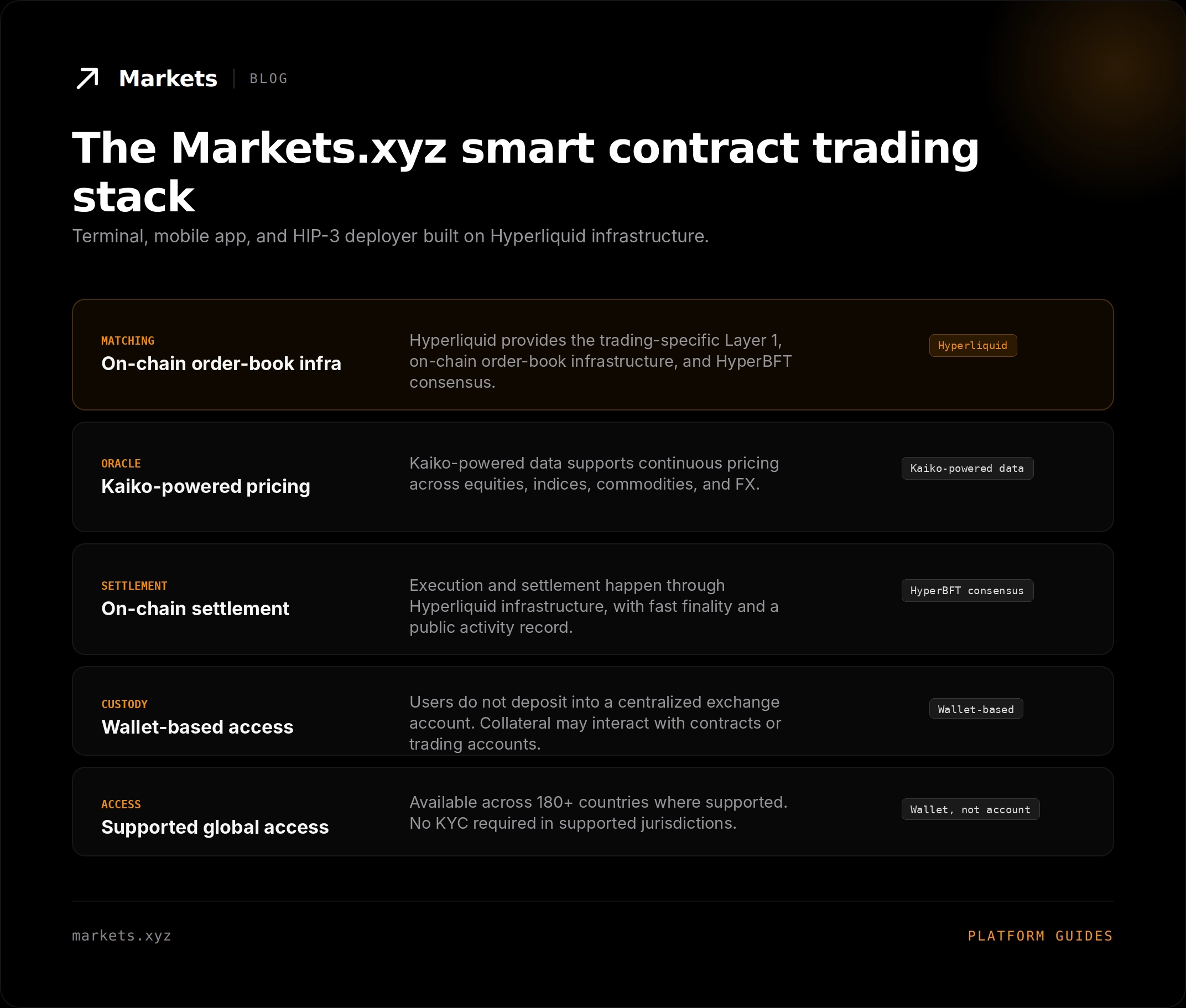

Hyperliquid is the clearest example: a purpose-built Layer 1 designed around high-performance trading, on-chain order books, and HyperBFT consensus. HIP-3 extends this by enabling deployers to launch new perpetual markets on Hyperliquid infrastructure. Markets.xyz sits above this stack as a trading terminal, mobile app, and HIP-3 deployer. Traders access the markets through the product layer, while the execution and settlement happen through Hyperliquid infrastructure.

The role of oracles in smart contract trading

Oracles are the bridge between the blockchain and the outside world. For any asset whose price is determined off-chain, the contract needs an oracle to know what to trade against. This is most obvious for traditional assets like equities, indices, and commodities, but it also applies to crypto prices from other venues.

Why oracles are essential

A smart contract that lets you trade an S&P 500 perpetual needs to know what the S&P 500 actually trades at. The blockchain doesn't natively know. The oracle is the component that delivers that information on-chain, continuously, in a way the contract can use to settle trades fairly. Without a reliable oracle, the contract can't tell whether your liquidation should trigger, what funding rate applies, or what your position is actually worth.

For 24/7 trading specifically, oracles do additional work. Traditional markets close. The oracle has to provide a continuous, fair price even during hours when the underlying market is offline. This requires synthesizing data from multiple sources, accounting for after-hours and futures pricing, and producing a number the contract can trust at any hour of any day.

Common oracle architectures

Push-based oracles publish updates continuously, with new price data written on-chain on a schedule. Pull-based oracles publish data on demand, when a contract requests an update. Many systems combine both. The key design decisions are how many data sources contribute, how those sources are aggregated, how often updates happen, and what fallback exists if the primary source fails.

Quality oracles use multi-source data aggregation, often with time-weighted averaging to reduce the influence of any single tick. Markets.xyz uses Kaiko-powered pricing for traditional assets, helping provide continuous pricing across equities, indices, commodities, and FX. For any smart contract trading platform, the quality of the oracle design is critical because it determines how positions are marked, liquidated, and settled.

Oracle risks and how good platforms mitigate them

Oracles can be manipulated. The classic attack involves moving the price on a venue the oracle reads, then exploiting positions on the platform that depends on that oracle. Good platforms mitigate this through multi-source feeds, deviation thresholds that flag suspicious updates, time-weighted averaging that smooths out short-term manipulation, and fallback feeds that kick in if the primary source becomes unreliable.

Evaluating an oracle is one of the most important steps in evaluating a smart contract trading platform. A platform with strong matching and settlement but a weak oracle is fundamentally not safe to use for any leveraged position. The oracle is where the most expensive attacks happen, and where the most engineering work goes into defending against them.

Risks specific to smart contract trading

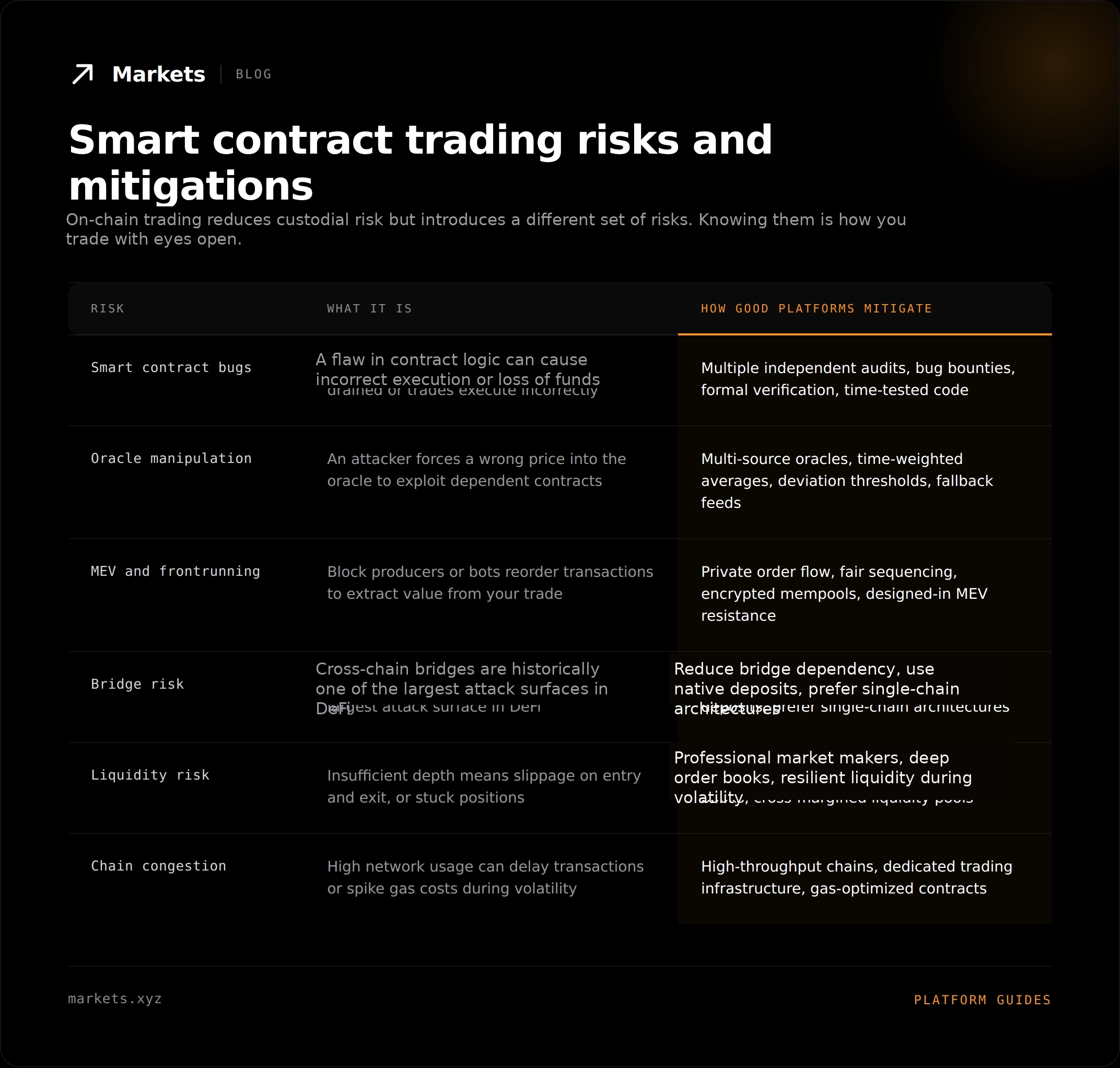

Smart contract trading reduces some risks dramatically and introduces new ones. The custody risk and counterparty risk that dominate centralized exchanges are largely absent. In their place are smart contract risk, oracle risk, MEV, and chain-level risks. Trading with eyes open means understanding what these are and how to evaluate the platform's defenses.

Smart contract bugs and audit quality

Smart contracts are software. Software can have bugs. A bug in a trading contract can let funds be drained, can let trades execute incorrectly, or can let attackers exploit edge cases for profit. The history of DeFi includes many examples of this. Audits help, but audits don't catch everything. Time-tested code, with significant value at stake and no major issues, is the strongest signal.

When evaluating a platform, look at the audit history. Multiple independent audits are better than one. Active bug bounty programs are better than no program. Code that's been live with meaningful TVL for many months or years carries more credibility than newly deployed contracts, regardless of how many audits the new code has.

Oracle manipulation attacks

If an attacker can manipulate the price feed an oracle uses, they can extract value from contracts that depend on that feed. The most common version is a flash-loan-driven attack, where an attacker borrows enough capital to move the price on a low-liquidity venue, then exploits the resulting wrong price on the target platform.

Strong oracle architectures defend against this with multi-source feeds, time-weighted averaging, and deviation guards. Trading on traditional assets like US500 is generally more resistant because the underlying markets have deep liquidity that's hard to manipulate even briefly. Trading on illiquid long-tail crypto is the most vulnerable scenario.

MEV and frontrunning

MEV stands for maximal extractable value. It refers to the ability of block producers, or sophisticated bots that work with block producers, to reorder transactions within a block in ways that extract value from regular users. The simplest version is frontrunning, where a bot sees your transaction in the mempool, places its own transaction ahead of yours, and captures the price improvement that should have gone to you.

Different chains and platforms address MEV differently. Some use private order flow, where transactions don't go through a public mempool. Some use fair sequencing protocols that constrain how block producers can order transactions. The right design depends on the kind of trading the platform supports. For active trading, MEV resistance is a meaningful quality differentiator.

Bridge and cross-chain infrastructure risks

Cross-chain bridges, which move assets between different blockchains, have historically been one of the largest attack surfaces in DeFi. Many of the largest single-incident DeFi losses have come from bridge exploits, not from trading contracts. Any platform that relies heavily on bridged assets inherits the risk of those bridges.

Single-chain platforms with native deposits reduce this specific attack surface because the trading path does not depend on cross-chain bridge infrastructure. That does not remove all infrastructure risk, but it avoids one of DeFi’s most historically expensive failure points.

Diligence check: Before deploying meaningful capital on any smart contract trading platform, verify three things. The audit history (multiple independent audits, with no major outstanding findings), the oracle architecture (multi-source, time-weighted, with defensible mitigations), and the chain-level characteristics (finality speed, throughput, and MEV resistance). A platform that's weak on any of these is not a platform for serious capital.

Trade on infrastructure built for transparency, security, and continuous markets. Start trading on markets.xyz.

Why smart contract trading enables 24/7 markets

The 24/7 nature of smart contract trading is not a feature added on top of the infrastructure. It's a consequence of the infrastructure itself. The reasons traditional markets close are operational, regulatory, and historical. None of those constraints apply to a smart contract running on a blockchain.

No central server to maintain

Traditional exchanges run on servers operated by the exchange company. Those servers need maintenance, patches, upgrades, and occasional restarts. Each one of those can become a window where the platform is degraded or offline.

Smart contracts do not depend on a single exchange-operated server. They run as part of the blockchain itself, which is maintained by a validator network. That does not make downtime impossible, but it changes the failure model from one company’s infrastructure to the resilience of the underlying chain.

No business hours to enforce

Centralized exchanges have employees, compliance processes, and customer support teams that operate around business processes. Even if the matching engine can run 24/7, the operational layer around the platform is still controlled by a company.

Smart contract platforms remove that company-operated approval layer from the execution path. The protocol does not sleep, take holidays, or wait for an operations team to approve trades.

No regional gatekeeping at the protocol level

Centralized exchanges restrict access by jurisdiction because they need to comply with regional regulations. They also require account approvals, identity checks, and ongoing compliance controls. Smart contract trading changes the access model from account-based to wallet-based.

Front-end interfaces may still apply geographic restrictions for compliance reasons, and specific systems can include protocol-level controls. But the underlying model is different from a centralized exchange deciding who can open an account, keep trading, or withdraw funds.

How Markets.xyz implements smart contract trading

Markets.xyz brings together three layers: a trading terminal, a mobile trading app, and a HIP-3 deployer built on Hyperliquid infrastructure. Hyperliquid provides the trading-specific Layer 1, on-chain order-book infrastructure, and HyperBFT consensus. HIP-3 allows deployers like Markets to launch and operate new perpetual markets on top of that infrastructure. Markets is the product layer traders use to access those markets.

Through Hyperliquid, Markets.xyz gives traders access to on-chain order-book execution, wallet-based access, and near-instant settlement. Through HIP-3, Markets can deploy and operate new perpetual markets across crypto, equities, indices, commodities, and FX. Through the terminal and mobile app, traders get a cleaner interface for accessing that infrastructure without having to think about the underlying stack.

Pricing for traditional assets is supported by Kaiko-powered data, helping provide continuous pricing across equities, indices, commodities, and FX. For crypto markets, pricing and execution depend on the underlying Hyperliquid market structure. The result is a trading product that gives users access to 24/7 markets through on-chain infrastructure.

Custody is self-custodial by default. Users do not deposit into a centralized exchange account or wait for an exchange operator to approve withdrawals. Depending on the market and trade type, collateral may interact with smart contracts or protocol-level trading accounts, but the custody model remains structurally different from a CEX: access is controlled by the user’s wallet, settlement is on-chain, and there is no centralized exchange balance standing between the trader and the system.

Access is available across 180+ countries, with no KYC required where Markets.xyz is supported. Front-end availability can still depend on jurisdiction and compliance restrictions. The wallet is the credential. The terminal is the interface. The underlying infrastructure is the venue.

You can trade supported markets through the same product layer. BTC perpetuals, US500, and other contracts use the same broader on-chain trading stack, with wallet-based access, on-chain settlement, and continuous market availability.

Self-custody, on-chain settlement, continuous markets, transparent execution. Start trading on markets.xyz.

Smart contract trading for different trader profiles

The same smart contract infrastructure serves very different trader profiles. Each profile gets different value from the architecture, but all of them benefit from the structural properties that smart contract trading provides.

The active retail trader

Active retail traders benefit from the lower fees, better execution, and broader asset access that smart contract platforms provide. Self-custody removes the platform risk that has historically wiped out account balances during exchange failures. Continuous access enables more setups across more hours. For traders who actively manage positions across multiple sessions, the structural advantages compound over time.

The DeFi-native trader

DeFi-native traders are already comfortable with self-custody wallets, on-chain transactions, and smart contract risk. For this audience, smart contract trading platforms are a natural extension of the rest of their DeFi stack. The wallet is the same, the security model is familiar, and the platform integrates with the broader on-chain ecosystem in ways centralized platforms cannot.

The institutional trader

Institutional traders care about counterparty risk in a structured way. Custody, settlement, and operational risk are quantifiable concerns with documented procedures. Smart contract platforms with wallet-based custody fundamentally change the risk model.

There is no centralized exchange account to become a bankruptcy claim and no private settlement ledger to reconcile against. The risks shift toward smart contract risk, oracle risk, custody operations, and chain-level risk, each of which can be evaluated with diligence.

What to look for in a smart contract trading platform

Not all smart contract trading platforms are built equally. The self-custody label alone is not enough to make a platform worth using. Before committing capital, evaluate the platform on the dimensions that actually determine whether the architecture works as advertised.

Audit quality is the first filter. Look for multiple independent audits, from reputable firms, with no major findings outstanding. Active bug bounty programs that pay out meaningful rewards are a strong positive signal. Time in production with significant value at stake and no critical incidents is the most persuasive single data point.

Oracle architecture is the second filter. A platform that depends on a single oracle source for prices is fragile. A platform that uses multiple sources with time-weighted aggregation and deviation guards is structurally more robust. For platforms that trade traditional assets 24/7, the oracle is doing the heaviest lifting and deserves the most scrutiny.

Settlement finality and chain throughput are the third filter. Slow chains create execution risk during volatility. Chains without enough throughput create congestion that delays trades or spikes costs. Trading-specific chains or high-performance general-purpose chains are the right base for active trading. Slower or less specialized infrastructure may work for slower strategies but will hurt active execution.

Liquidity and execution quality are the fourth filter. Verifiable infrastructure does not help if the order book is empty. Look for platforms with professional market makers, deep order books across the assets you trade, and a track record of holding execution quality during volatile periods.

Platform checklist: Audit history, oracle architecture, settlement infrastructure, liquidity depth, and operational transparency. A platform that's strong on all five is a platform worth using for serious capital. A platform that's weak on any single one is a platform you should be cautious about, regardless of how many of the other boxes it checks.

Frequently asked questions

The most common questions traders ask about smart contract trading, answered without the marketing gloss.

Is smart contract trading the same as DEX trading? Effectively yes, though the term DEX has historically been associated with AMM-based platforms like Uniswap. Smart contract trading is a broader term that includes order book platforms, AMMs, and hybrid models. Any platform where trades execute through verifiable on-chain code rather than a centralized matching engine is a smart contract trading platform.

How does my money stay safe in a smart contract trade? Through self-custody. Your funds remain in your own wallet at all times. The smart contract has permission to execute trades and update positions, but it cannot move your funds outside your wallet without your signature. Even if the platform's interface were compromised, an attacker would still need your private key to access your underlying balance.

Are smart contracts ever hacked? Yes. Smart contract bugs and exploits do happen, and have caused major losses across DeFi. Good platforms minimize this risk through multiple audits, formal verification, bug bounty programs, and time-tested code. The risk is real and worth understanding, but it's a different kind of risk from custodial failure on a centralized exchange. Both are quantifiable. Self-custody platforms make different trade-offs, not zero trade-offs.

Why is gas relevant in smart contract trading? Gas is the fee paid to the blockchain for processing a transaction. On general-purpose chains, gas costs can spike during congestion, making small trades uneconomic. Trading-specific chains are designed to keep gas low and predictable. On Hyperliquid HIP-3, which Markets.xyz is built on, transaction costs are negligible by design, even during volatility.

Can I get the same execution quality as on a CEX? Yes, on platforms built for it. The first generation of DEXs had visible execution gaps versus CEXs. The current generation, built on trading-specific infrastructure with professional market makers and on-chain order books, matches or exceeds CEX execution quality for most trade sizes. The gap that used to exist has largely closed for serious platforms.

What happens if the oracle fails or gives a wrong price? Good platforms have multiple defenses. Multi-source oracles mean a single source going wrong doesn't immediately affect prices. Time-weighted averaging smooths out short-term anomalies. Deviation thresholds flag suspicious updates. Fallback feeds kick in if the primary source becomes unreliable. Catastrophic oracle failure is rare on well-designed systems and is typically the largest single design priority of the platform team.

Is smart contract trading legal in my country? Regulations vary significantly by jurisdiction. Smart contract trading platforms generally operate as protocols, and many use front-end interfaces that apply geographic restrictions for compliance. Markets.xyz is available in 180+ countries but is not available to residents of the United States, the United Kingdom, or the province of Ontario in Canada. Confirm local regulations before using any platform.

Conclusion

Smart contract trading is not a marginal upgrade to traditional exchanges. It’s a different model. Custody moves from exchange-controlled accounts toward self-custody. Settlement moves from internal ledgers to blockchain infrastructure. Execution moves from private exchange systems toward on-chain trading infrastructure with a public activity record. Access moves from account approval to wallet-based interaction. Each of these changes has structural consequences, and together they create a fundamentally different trading experience.

The architecture is not free of risks. Smart contract bugs, oracle manipulation, MEV, and chain-level risks all need to be understood and evaluated. Good platforms invest heavily in mitigating each of them. The trader's job is to evaluate the mitigations and decide whether the platform's specific implementation is one they trust enough to deploy capital on.

Done well, smart contract trading delivers something centralized exchanges structurally cannot: wallet-based access, on-chain settlement, continuous markets, and a trading record that can be independently inspected. The future of trading will not be defined only by faster matching engines. It will be defined by who controls custody, where settlement happens, and whether traders can verify the system they trade on.

Trade on infrastructure built for the next era of markets. Start trading on markets.xyz.

Risk disclaimer: Trading involves substantial risk, including the possible loss of principal. Smart contract trading carries specific risks including smart contract vulnerabilities, oracle manipulation, and chain-level risks, in addition to standard market risks. Leverage amplifies both gains and losses. Past performance is not indicative of future results. Markets.xyz is not available to residents of the United States, the United Kingdom, or the province of Ontario in Canada. Full terms, conditions, and risk disclosures are available at markets.xyz. Information in this article is for educational purposes only and does not constitute financial, investment, or trading advice.