Learn about trading

Mark price

Last updated

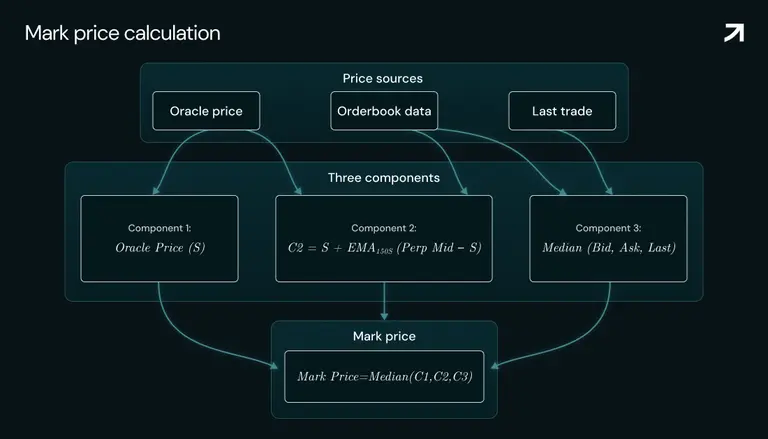

The mark price is a manipulation-resistant internal valuation used for margining, liquidations, stop/limit triggers, and unrealized P&L. It is calculated as the median of three independently derived components.

Mark price construction

Mark price formula:

Component | Formula | Purpose |

|---|---|---|

| Anchors to real-world external value | |

Smoothly incorporates orderbook sentiment

| ||

| Reflects current on-chain market |

This allows mark price to track orderbook dynamics while staying anchored to the oracle.

Why median? (protection mechanism)

Scenario | C₁ | C₂ | C₃ | Mark price |

|---|---|---|---|---|

Normal market | $100 | $100.50 | $100.25 | $100.25 |

Oracle manipulation | $105 | $100.50 | $100.25 | $100.50 |

Orderbook manipulation | $100 | $100.50 | $95.00 | $100 |

- Median prevents any single component from dominating

- Manipulation of one source doesn't skew the mark price

- 150-second EMA dampens sudden orderbook moves

Fixed bounds

To prevent extreme deviations from the oracle, mark price is constrained within calculated bounds.

Mark price bounds use a fixed percentage based on maximum leverage:

Max leverage | Bound |

|---|---|

50× | ±2% |

20× | ±5% |

10× | ±10% |

Example: For an asset with 10x max leverage and oracle price of $100, mark price is bounded between $90 and $110.

Purpose of bounds

- Prevent liquidation cascades caused by temporary distortions

- Maintain alignment with external reference pricing

- Provide predictable risk envelopes

- Reduce systemic instability during volatility

Bounds apply to the mark price, not the last trade price.

Note that Markets by Kinetiq currently employs a "soft" bounding, which means that although Mark and Oracle are fixed at the limit (protecting from liquidations), trading is allowed beyond it. This approach is taken to allow traders to continue to open and close positions, with funding acting as an incentive to bring price back towards the limit.

Planned enhancement: dynamic expanding bounds

Future versions will implement dynamic bounds that adapt to market conditions:

Parameter | Value | Description |

|---|---|---|

Initial width | 0.66 × (1/L) | Starts at 66% of fixed bound (tighter) |

Behavior | Expanding | Widens during sustained price moves |

Cap | 1/(1.5 × L) | Maximum expansion limit |

This allows tighter bounds during normal conditions while accommodating legitimate large moves.

Trader considerations

What to watch | What it means |

|---|---|

Mark vs last trade spread | Large spread = protection system active |

Oracle vs perp spread | Indicates funding rate direction |

Weekend pricing | Uses internal pricing; may have wider bounds |

Near ex-dividend dates | Oracle adjusts for dividend; understand impact on funding |

Pro tip: Your liquidation price is based on mark price, not the last traded price. In volatile conditions, check the mark-to-last-trade spread. If you see a flash crash in last trade but mark price stays stable, your position is safe.

On this page